You’ve just arrived in a new country after a long flight. Check-in at the hotel seems smooth—until the payment terminal flashes a message you weren’t expecting:

“Payment Declined.”

You try again. Same result. Your card worked perfectly just hours ago.

If this has happened to you, you’re not alone. Being declined abroad is far more common than most travelers realize. The frustrating part? In many cases, it’s not about your balance or funds—it’s about systems interpreting risk differently in international contexts.

Let’s explore what’s happening behind the scenes and how you can avoid this scenario.

Why Does My Bank Decline My Card Abroad?

Banks use automated fraud detection to protect you from suspicious activity. When your card suddenly appears in a country you don’t usually visit, it can trigger a risk alert.

This often happens when you make your first overseas purchase, attempt a high-value transaction, or perform several payments in quick succession. Even legitimate transactions can be blocked as a precaution.

Many banks allow you to set travel notifications in advance, but travelers often only realize this after a decline occurs.

Can Merchants Reject My Card Even If My Bank Approves It?

Yes. Payment failures aren’t always about your bank. Merchants or payment processors may impose restrictions based on card issuing country or type.

Foreign-issued cards, prepaid cards, and some virtual cards are more likely to be rejected. Hotels, car rentals, subscription platforms, and ticketing systems often enforce these rules to manage fraud risk.

Even if your bank approves the payment, the merchant can still decline it at the final step.

Why Does My Card Fail Due to Pre-Authorization Holds?

Certain businesses, especially hotels and rental services, place temporary holds on more than the final amount. This usually includes room fees plus a security deposit.

If your available balance doesn’t cover the full authorization amount, the transaction can fail instantly—even if your actual charge is much lower. Many travelers are surprised because the final bill seems reasonable, but the pre-authorization requirement is higher.

Are Some Cards More Likely to Be Declined?

Not all cards are treated equally in global payment systems. Prepaid cards, virtual cards without proper billing verification, or cards that don’t support 3D Secure authentication are at higher risk.

This is especially common with AI subscriptions, digital advertising platforms, and SaaS tools, where fraud detection is strict. Choosing a card that supports international payments and 3D Secure reduces the likelihood of a decline.

Could a Billing Address Issue Cause My Card to Be Rejected?

Yes. Billing address mismatches are a subtle but common reason for declines. If the address linked to your card doesn’t match the merchant’s validation requirements—or isn’t formatted correctly for international processing—the transaction may be automatically declined.

Why Do Multiple Payment Attempts Trigger a Decline?

It’s natural to retry immediately after a failed payment. However, multiple rapid attempts can trigger security systems. Payment platforms may interpret repeated attempts as card testing or suspicious activity, temporarily blocking the card until the system resets its risk evaluation.

How Do Real-Time Fraud Scoring Systems Affect My Transactions?

Modern payment networks use real-time fraud scoring, evaluating multiple signals including device fingerprint, IP location, spending patterns, and merchant category risk.

Even valid, funded cards can be declined if the risk score is too high. That’s why two identical cards may behave differently at the same merchant.

How Can I Prevent My Card From Being Declined Abroad?

Preparation is key. To reduce the risk:

- Notify your bank of upcoming travel.

- Avoid making large transactions abroad for the first time.

- Keep backup payment methods handy.

- Ensure your card supports international payments and 3D Secure.

- Test your card with a small online purchase before departure.

Why Virtual Cards Are a Smart Choice for Global Payments

Frequent travelers, freelancers, and digital workers increasingly turn to virtual cards for better payment control.

Virtual cards can:

- Be issued instantly

- Have fixed spending limits

- Be frozen or closed anytime

- Reduce exposure of your main account

Platforms like BUVEI make cross-border payments predictable, especially in high-failure scenarios like travel bookings, AI subscriptions, ad accounts, and SaaS tools.

Step-by-Step: Using BUVEI Virtual Cards

- Sign Up and Verify– Click “Start Free” to create or log in to your BUVEI account.

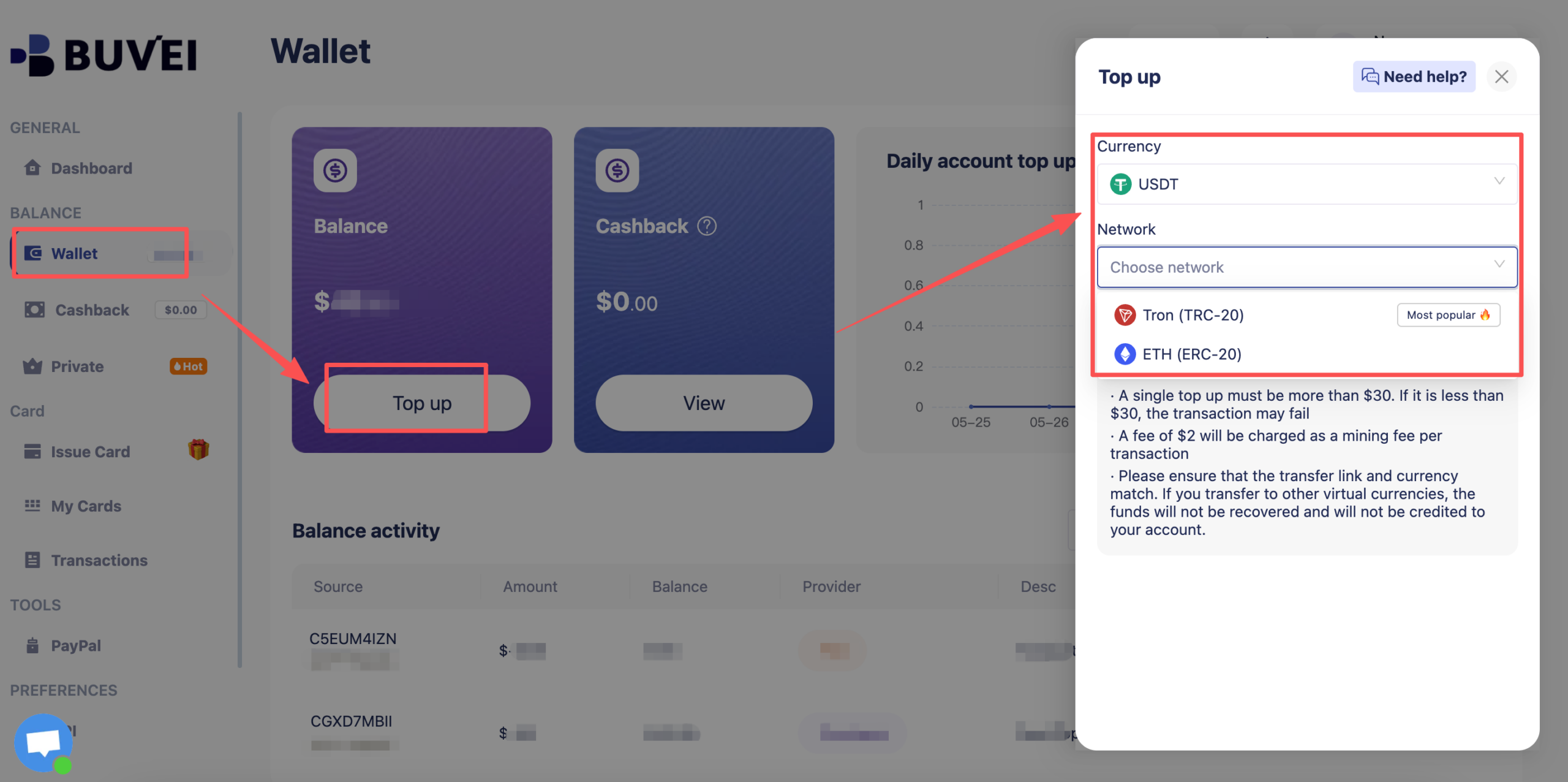

- Fund Your Wallet– Add funds using USDT (TRC20/ERC20) or other supported stablecoins.

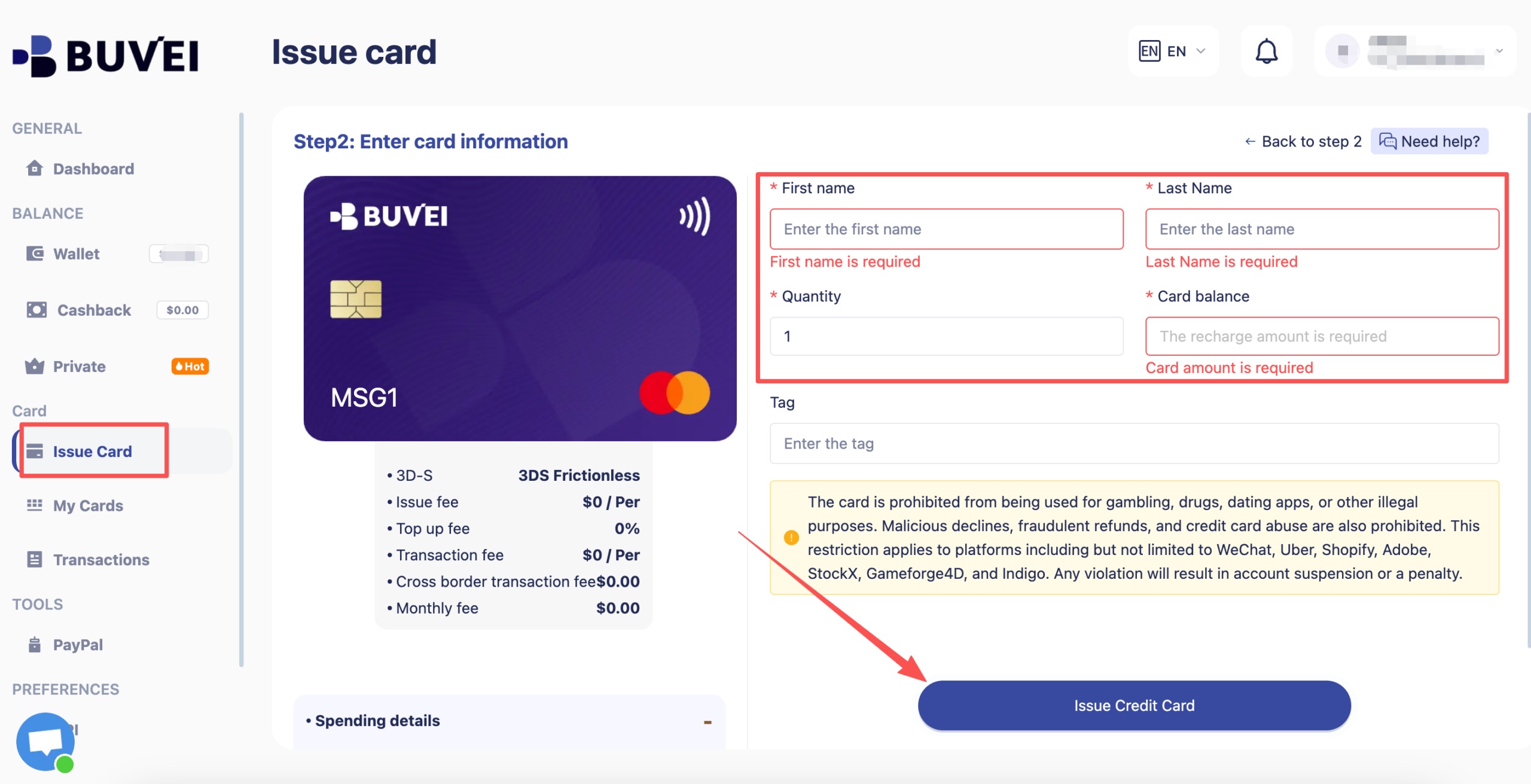

- Create Your Virtual Card– Fill in card details, amount, and quantity, then issue the card.

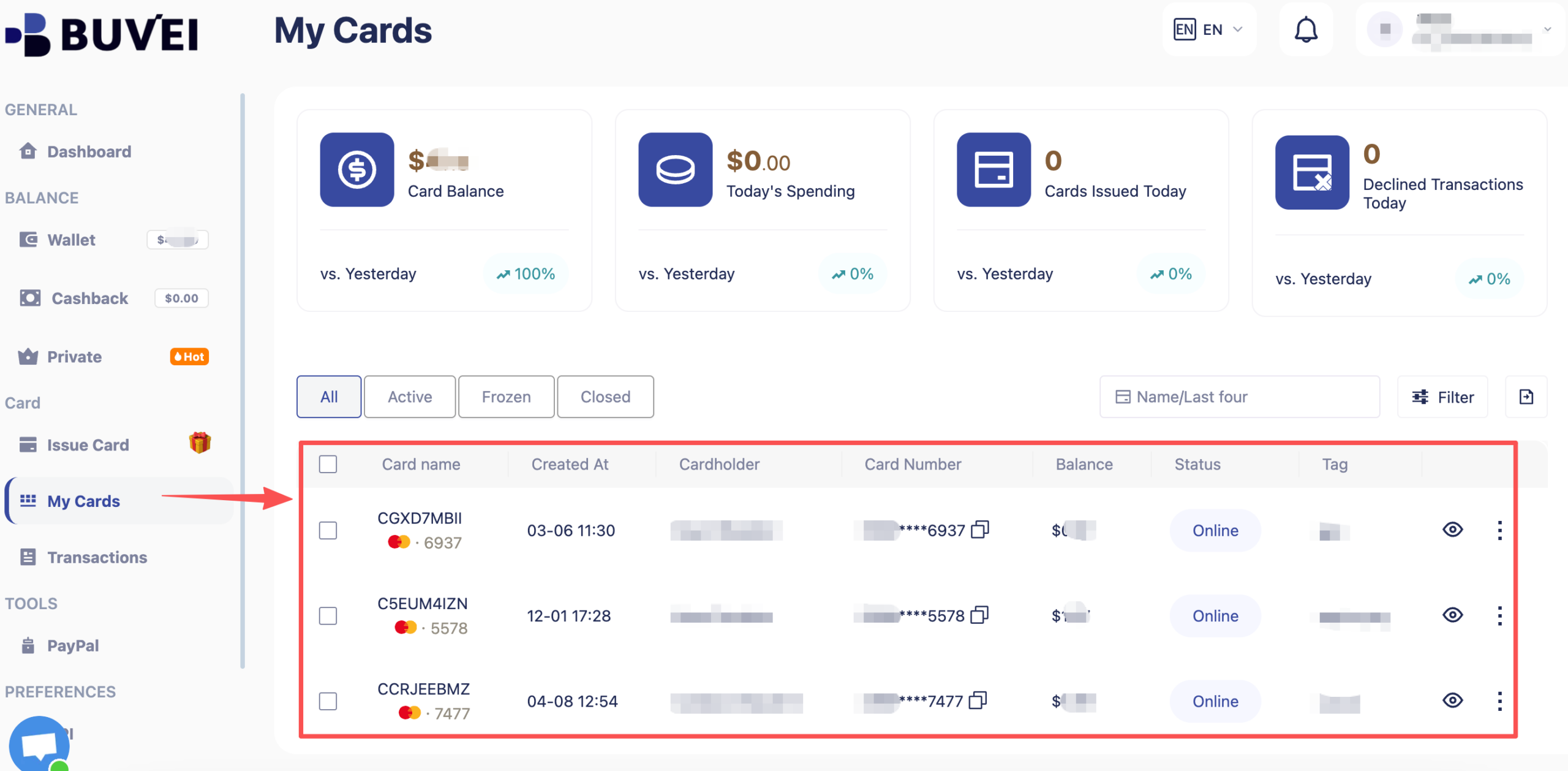

- View Card Details– Check card number, expiration date, and CVV under “My Cards.”

- Monitor and Manage– Track spending and transactions under “Transactions.”

Final Thoughts

Being declined abroad can feel like a financial problem, but it’s actually a mismatch between global payment systems and risk control logic.

Understanding the system allows you to prepare effectively. With the right cards and virtual payment tools like BUVEI, you can make international payments as reliably as you plan your trip.