Every time a customer swipes a card, there's a hidden cost that quietly moves in the background. While this fee is typically paid by merchants, it often ends up reflected in the price consumers pay. This behind-the-scenes cost is known as the interchange fee—one of the most fundamental yet misunderstood components of today’s global payment ecosystem.

In this article, we’ll unpack how interchange fees work, who pays whom, and how virtual card platforms like Buvei are optimizing this cost structure to help small and medium-sized businesses (SMBs) take control of their payments.

What Is an Interchange Fee?

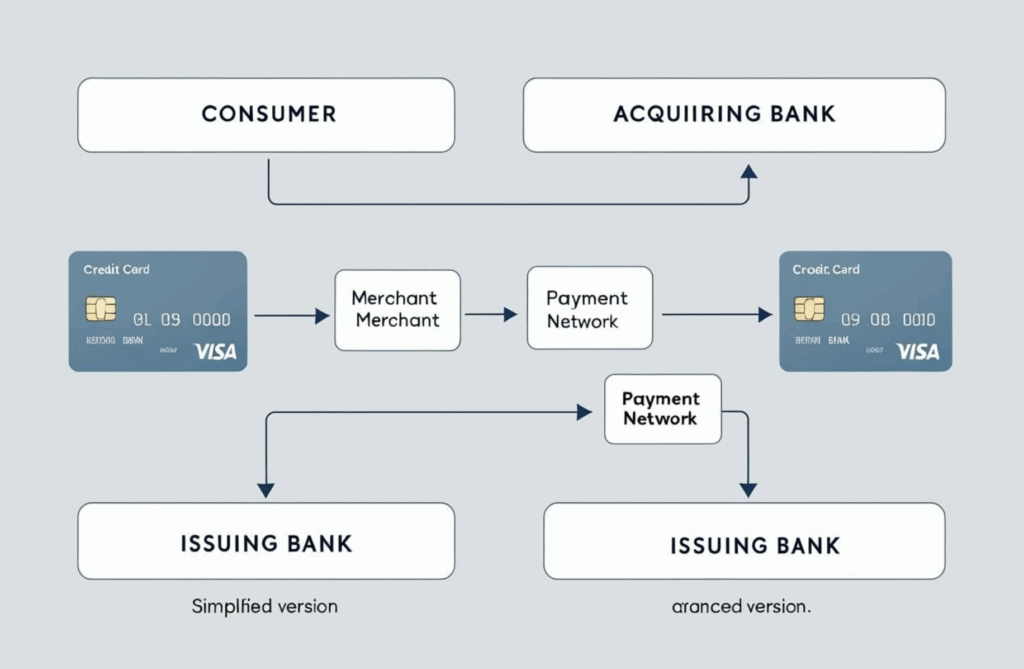

An interchange fee is a fee paid by the acquiring bank (the merchant’s bank) to the issuing bank (the cardholder’s bank). It compensates the issuer for handling payment risks, providing credit, and facilitating the transaction process.

In simpler terms, when a customer makes a card payment, this fee is deducted from the merchant’s end and passed on to the cardholder’s bank. While end-users don't pay this fee directly, it’s typically baked into the merchant’s pricing model.

📌 Example: If you pay $100 via Visa at an online store, roughly 1.5% to 2% ($1.50–$2.00) goes to your card issuer as interchange, deducted from what the merchant ultimately receives.

Where Does the Swipe Fee Go? A Breakdown

A typical card payment involves several cost components:

| Fee Type | Typical Range | Recipient | Purpose |

| Interchange Fee | 1.0% – 2.5% | Issuing Bank | Compensates risk, credit, and processing |

| Network Fee | 0.05% – 0.15% | Card Network (Visa, etc.) | Infrastructure and fraud monitoring |

| Processing/Markup Fee | 0.2% – 1.0% | PSPs / Virtual Card Platforms | Platform services, API access, support |

⚠️ These percentages can vary significantly depending on factors like country, card type (debit, credit, commercial), and transaction channel (online vs. in-store).

Who Sets Interchange Rates?

Interchange fees are typically set by card networks like Visa or Mastercard, and they vary based on:

-

Transaction channel: Online (card-not-present) transactions carry higher risk and thus higher fees than in-store transactions.

-

Card type: Commercial and credit cards often have higher fees than personal debit cards.

-

Region: In the U.S. and EU, interchange fees are tightly regulated. In emerging markets, they can vary widely.

-

Merchant category (MCC): High-risk categories like digital ads or adult services often face premium interchange fees.

That’s why the card BIN (Bank Identification Number) and issuing structure a virtual card platform uses will significantly impact your underlying transaction cost.

How Virtual Card Platforms Optimize Interchange

Virtual card providers like Buvei sit at the middle of the value chain and play an essential role in balancing cost and usability.

-

Upstream: We work with licensed BIN sponsors and issuing banks to negotiate base interchange access.

-

Midstream: We bundle compliance, risk control, and technical operations into a streamlined offering.

-

Downstream: We offer end users (merchants, teams, finance leaders) a secure, transparent, and configurable way to manage cards and costs.

Unfortunately, many virtual card providers hide these costs or implement tiered pricing models that make it hard for businesses to assess true expenses.

At Buvei, we believe in:

-

Transparent pricing: Different fee structures for ads, subscriptions, one-time use, etc.

-

No hidden charges: No account reserve fees, silent activations, or binding lock-ins.

-

Custom spend rules: Time-based limits, category restrictions, and usage caps to reduce unnecessary exposure to high interchange.

📌 Example: If you only need a card to bind a SaaS tool once, Buvei lets you issue a time-limited, low-limit virtual card—keeping risk and fees minimal.

Making Payment Fees Transparent and Controllable

For small and growing teams, managing interchange and platform markups can be overwhelming. Traditional providers often lack flexibility and transparency.

Buvei is built differently, offering:

-

Dynamic BIN routing based on the business case and region

-

Smart fee matching for high-risk use cases like digital ads or cross-border SaaS

-

API-based transaction insights, so your finance team can export and reconcile with confidence

We believe payment infrastructure shouldn’t be a black box—it should be a growth enabler.

Understanding Interchange Starts with Awareness

There’s no such thing as a “free” payment. But when businesses understand how interchange fees work, they’re better equipped to negotiate terms, choose partners wisely, and manage spending with greater control.

With Buvei, we make it possible to see, calculate, and optimize your payment costs—one card at a time.

📌 Learn more about Buvei’s virtual card solutions and pricing structure: https://buvei.com