Virtual Credit Cards (VCCs) are now foundational infrastructure for digital payments. From SaaS subscriptions and advertising platforms to travel bookings and cross-border eCommerce, VCC systems power billions of dollars in online transactions each year.

But behind the simple 16-digit number is a sophisticated ecosystem involving issuers, processors, networks, BIN management, APIs, and compliance layers.

This guide explains how the VCC system works from the ground up.

What a VCC Card System Is

A VCC (Virtual Credit Card) system is a digital card issuance framework that allows users or businesses to generate card numbers without issuing physical plastic cards.

A VCC system typically includes:

-

Card number generation

-

CVV and expiration assignment

-

Spending limits and controls

-

Authorization routing

-

Transaction monitoring

-

Card lifecycle management (freeze, close, renew)

Unlike traditional bank cards, virtual cards are often:

-

Created instantly

-

Used for specific merchants or purposes

-

Configurable with custom limits

The card itself is only the visible layer. The real system operates behind the scenes through payment networks and financial infrastructure.

Three Main Virtual Card Architectures (Issuer, Processor, Program Manager)

The VCC ecosystem is built on three core structural roles:

1. Issuer

The issuer is a licensed financial institution (bank or EMI) that:

-

Holds regulatory approval

-

Owns the BIN (Bank Identification Number)

-

Legally issues the card

-

Assumes compliance responsibilities

Without an issuer, no virtual card can legally exist.

2. Processor

The processor handles:

-

Transaction authorization routing

-

Fraud monitoring

-

Settlement processing

-

Card lifecycle services

When a transaction is made, the processor communicates between:

-

Merchant

-

Acquiring bank

-

Card network (Visa/Mastercard)

-

Issuer

Processors ensure technical connectivity and real-time approval logic.

3. Program Manager

The program manager builds the user-facing layer:

-

Dashboard or web interface

-

API access

-

Card creation logic

-

Spending control tools

-

Reporting and analytics

Program managers partner with issuers and processors to deliver branded virtual card services.

In many fintech platforms, users only see the program manager — but the issuer and processor operate behind the scenes.

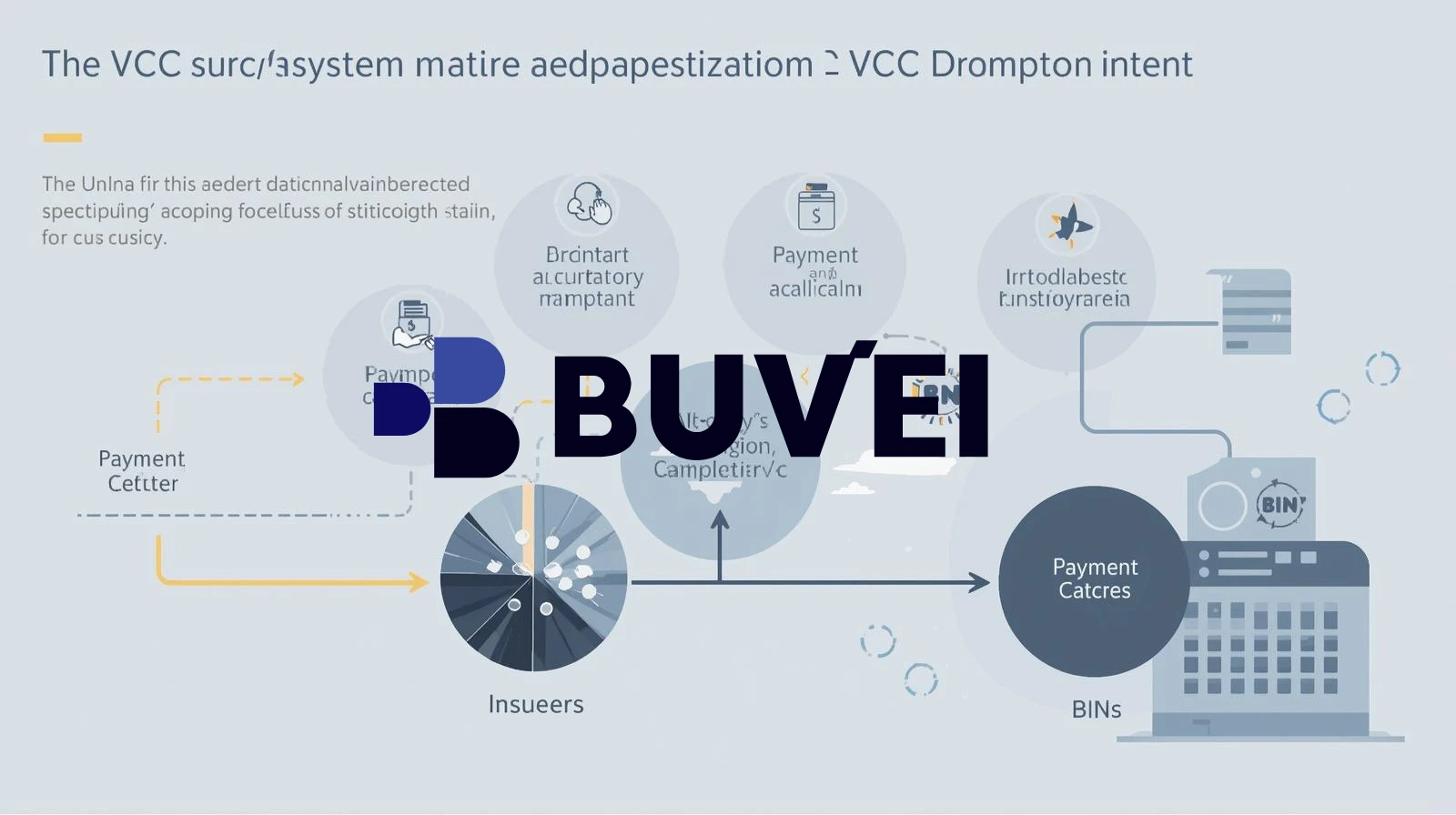

Payment Channels, BINs, and Authorization Flow

Understanding authorization flow is key to understanding VCC performance.

BIN (Bank Identification Number)

The first 6–8 digits of a card identify:

-

Issuer

-

Country

-

Card network (Visa or Mastercard)

-

Card type (credit, debit, prepaid)

BIN reputation significantly affects approval rates, especially for:

-

Advertising platforms

-

SaaS subscriptions

-

Cross-border merchants

A clean BIN with strong compliance history tends to experience fewer declines.

Authorization Flow

When a virtual card is used:

-

Merchant sends transaction request to acquiring bank

-

Acquirer forwards request to card network

-

Card network routes to issuer processor

-

Issuer evaluates:

-

Available balance

-

Risk signals

-

Merchant category

-

Velocity checks

-

-

Approval or decline is returned

This entire process typically occurs in milliseconds.

Declines can occur at multiple levels:

-

Merchant risk engine

-

Acquirer filters

-

Network rules

-

Issuer fraud controls

The virtual card provider influences issuer-level approvals but not always merchant-level decisions.

API-Based Card Issuing and Backend Management

Modern VCC systems are heavily API-driven.

API-based issuing allows:

-

Instant card creation

-

Automated limit adjustments

-

Merchant-specific cards

-

Programmatic freezing or closing

-

Real-time transaction webhooks

-

Bulk card generation

For businesses managing:

-

Multiple ad accounts

-

Subscription-heavy SaaS stacks

-

Affiliate campaigns

-

Travel bookings

API control enables scalable financial operations.

Backend management systems also include:

-

Ledger accounting

-

Currency conversion logic

-

Balance tracking

-

Compliance monitoring

-

Anti-money laundering (AML) screening

The complexity of the backend determines system stability and decline rates.

How Platforms Like Buvei Deliver Virtual Card Services

Platforms like Buvei operate as program managers within the VCC ecosystem.

Their role typically includes:

-

Partnering with licensed issuers

-

Integrating with payment processors

-

Providing user dashboards and APIs

-

Managing card creation and spending limits

-

Supporting cross-border online payments

Buvei virtual cards are designed for:

-

SaaS subscriptions

-

Advertising platforms

-

AI tool payments

-

Cross-border digital services

By combining issuer infrastructure with user-facing tools, platforms like Buvei make enterprise-grade virtual card infrastructure accessible to freelancers, marketers, startups, and digital operators.

Final Thoughts

The VCC system is not just a digital card number — it is a multi-layered financial infrastructure involving:

-

Issuers

-

Processors

-

Program managers

-

Payment networks

-

Risk engines

-

Compliance frameworks

In 2026, virtual cards are not just a convenience — they are programmable financial infrastructure powering the global digital economy.