In today's digital-first commerce landscape, every step in the payment flow has the potential to make or break a transaction. Among the most critical yet often overlooked stages is card authorization — the decision point where a card-issuing bank accepts or declines a transaction. For merchants and platforms, optimizing this step can mean the difference between a completed purchase and an abandoned cart.

Why Authorization Rates Matter

Authorization rate refers to the percentage of card payment attempts that are successfully approved. Across industries, a 1% improvement in authorization rates can translate to millions in recovered revenue. Yet, according to Visa (2024), average global auth rates hover between 78% and 85%, leaving significant room for optimization.

High decline rates don’t just hurt revenue; they also:

-

Erode consumer trust

-

Trigger false positives in fraud systems

-

Increase customer support load

Improving this metric requires a deep understanding of issuer behavior, real-time risk scoring, and data-enriched transaction routing.

Key Factors Affecting Authorization Outcomes

1. Issuer Logic and Risk Models

Issuing banks make decisions based on internal risk models, which factor in geolocation, purchase size, card usage patterns, and more. Transactions that deviate from expected behavior can trigger automatic declines, even if they are legitimate.

What helps:

-

Sending enriched transaction metadata (e.g., MCC, merchant name, device ID)

-

Aligning with issuer preferences through partnership or BIN-level insights

2. Real-Time Risk Scoring

Leading payment platforms now apply their own machine learning models to assess fraud risk in real-time before routing to issuers. By reducing the volume of flagged transactions, platforms can improve issuer confidence and approval rates.

Example:

-

A smart risk engine may downgrade a transaction from "high" to "medium" risk if device fingerprinting matches previous behavior.

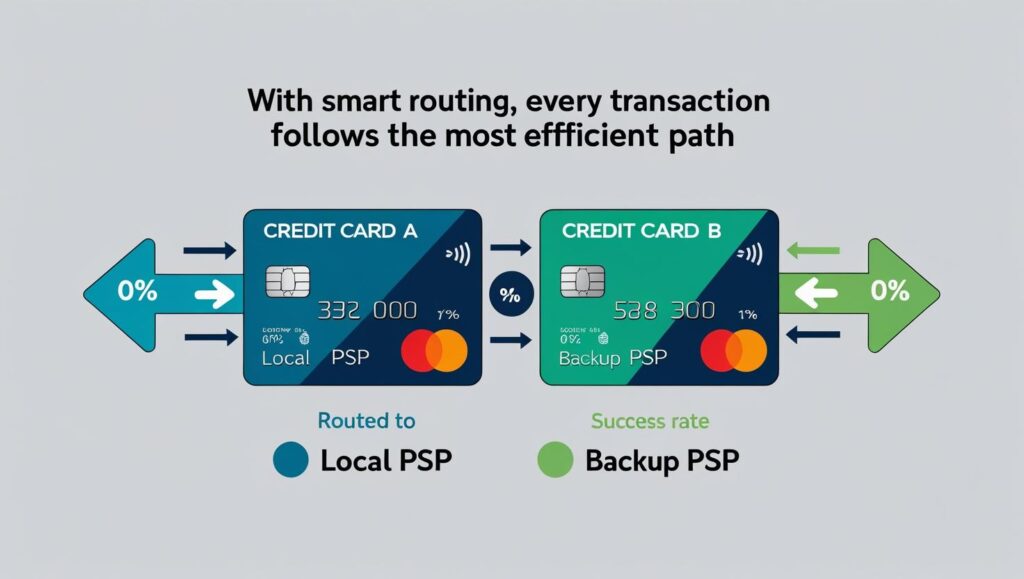

3. BIN Intelligence and Smart Routing

Card BINs (Bank Identification Numbers) provide key insights into issuer behavior. Some issuers favor specific routing paths or have known latency/failure patterns. Using BIN-level intelligence, payment systems can:

-

Route transactions to the optimal acquiring path

-

Retry through alternative processors if soft-declined

The Rise of Network Tokenization

Tokenization is no longer just a security feature. Network tokens — issued and managed by schemes like Visa and Mastercard — are now shown to increase authorization rates by up to 3%, especially in recurring or cross-border transactions.

Why it works:

-

Tokens are regularly refreshed and recognized by issuers

-

Device binding and contextual data increase issuer trust

Platforms that have adopted network tokenization are seeing fewer declines due to expired or reissued cards.

Buvei Perspective: Embedded Flexibility in Authorization Design

At Buvei, we believe that smarter authorization starts with more granular control and visibility. Our virtual card infrastructure enables:

-

Custom spend rules: Tailor authorization by merchant, MCC, or time

-

Card-level routing insights: Monitor auth success by issuer and region

This helps businesses, especially in the B2B and cross-border space, adapt to dynamic authorization patterns in real-time, while keeping fraud low and conversion high.

Actionable Steps for Merchants and Platforms

-

Monitor Auth Rates by Issuer & Geography

-

Identify patterns of soft declines or time-based rejections

-

-

Leverage Network Tokens Where Possible

-

Especially for subscription or returning customers

-

-

Implement Smart Retry Logic

-

Don’t just retry failed payments blindly; route with context

-

-

Partner with Payment Providers Offering BIN-Level Optimization

-

Choose PSPs that share transparent auth rate metrics

-

Looking Ahead: Authorization-as-a-Service?

In the future, we may see "authorization" abstracted into its own infrastructure layer. Similar to fraud engines or token vaults, Authorization-as-a-Service could offer plug-and-play optimization, tailored to business models, risk profiles, and even customer behavior.

For now, investing in the right stack — and partners like Buvei — is the clearest way to future-proof your payments strategy.