Tokenization: A Cornerstone of Secure Payments

As digital payments continue to scale globally, tokenization has become a vital tool in combating fraud and safeguarding sensitive data. According to Visa’s 2024 report, tokenization can reduce payment fraud by up to 60%. Yet, over 70% of merchants have yet to fully leverage its capabilities.

By replacing sensitive card data with a secure, non-reversible token, this technology ensures that real card numbers are never exposed during transactions — enhancing both consumer trust and payment security.

How Tokenization Works — And Its Different Forms

Tokenization workflow:

-

Data entry: The user enters their card number (e.g., 4111 1111 1111 1111) at checkout

-

Token request: The merchant system sends the card data to a Token Service Provider (TSP)

-

Token generation: The TSP returns a secure token (e.g., tok_789e12fg45hi67)

-

Transaction processing: The token is used like a real card number to complete the transaction via the payment network

Key features:

✅ Irreversibility – Tokens are mathematically unrelated to the original PAN

✅ Scoped usage – Tokens can be bound to specific merchants or devices (e.g., Apple Pay)

Types of tokens:

| Token Type | Use Case | Example Token |

| Payment Token | Subscription services | tok_v4s9... |

| Gateway Token | PSP-specific (e.g., Stripe) | pi_3LN... |

| Network Token | Issuer-backed (Visa, Mastercard) | 4895 12XX XXXX 9012 |

Regulatory & Compliance Benefits

Reduced PCI DSS Scope: Tokenization can shrink PCI compliance requirements by up to 80% (TokenEx, 2023). Since only the TSP handles raw card data, merchants avoid direct exposure to sensitive information.

GDPR & PSD2 Alignment: Under GDPR Article 4(5), tokens are categorized as pseudonymized data. Additionally, network token transactions may qualify for PSD2’s Strong Customer Authentication (SCA) exemptions.

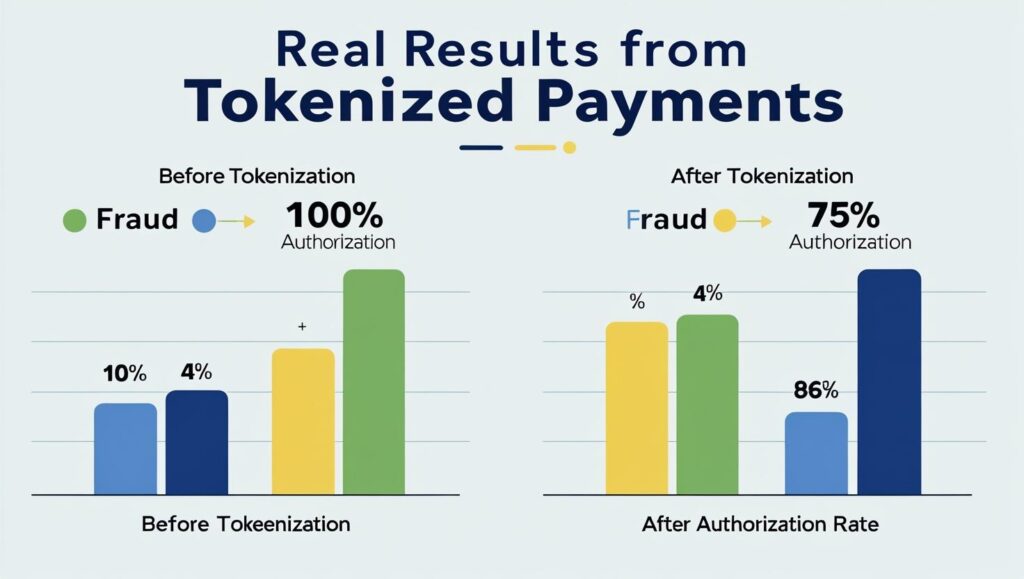

Business Impact: Fraud Reduction & User Experience

Case Study: After implementing network tokenization, a European travel platform reported:

-

58% reduction in fraudulent orders

-

11% increase in approval rates (due to higher issuer trust in tokenized payments)

Token vaults support one-click checkout experiences without storing card numbers, and network tokens help bypass regional card restrictions — especially useful in cross-border transactions.

-

Implementation Guidelines

For PSPs (Payment Service Providers):

-

Partner with PCI Level 1-certified Token Service Providers

-

Ensure API frameworks comply with EMVCo standards (especially for mobile wallets)

-

Implement lifecycle management for token expiration and revocation

For merchants:

-

Require tokenization support from PSPs

-

Audit token request logs quarterly to detect anomalies

With solutions like Buvei’s virtual card infrastructure, businesses can more easily integrate tokenization into their payment stack — improving global transaction security and flexibility with minimal development overhead.

Looking Ahead: The Future of Tokenization

Emerging trends are set to expand the role of tokenization:

-

CBDCs: The European Central Bank’s digital euro pilot includes tokenized architecture

-

Biometric linking: Mastercard plans to pilot facial and voice biometric-token pairing by 2025