As digital payments accelerate globally, virtual cards have become indispensable for high-frequency use cases such as ad payments, SaaS subscriptions, and cross-border e-commerce. But behind every successful transaction lies a complex, highly orchestrated system. This article breaks down the core technical architecture powering virtual cards and explains how platforms like Buvei implement efficient, secure infrastructure for modern business needs.

Key Players in the Virtual Card Ecosystem

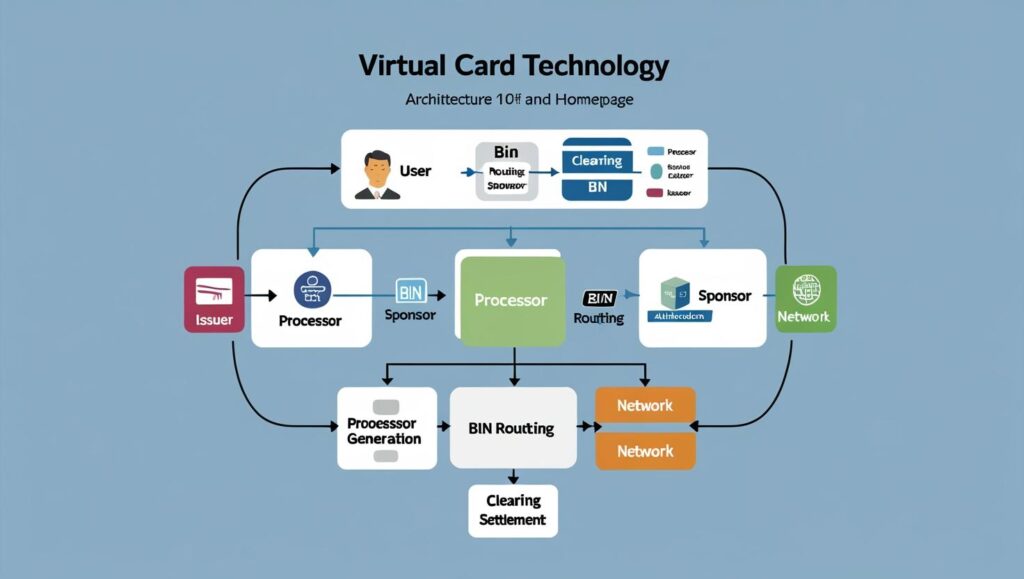

The lifecycle of a virtual card typically involves the following actors:

-

Issuer: Licensed banks or fintech companies that issue cards and manage user funds.

-

BIN Sponsor: Provides Bank Identification Number (BIN) resources and facilitates network access.

-

Card Network: Schemes like Mastercard and Visa that handle transaction routing and settlement.

-

Processor: Offers backend services like authorization, routing, risk evaluation, and limit controls.

-

Cardholder: The end user (individual or business) utilizing the virtual card for online payments.

💡 Tip: Some platforms consolidate multiple roles to ensure faster service and more control. For example, Buvei.com not only supports multi-currency wallets and Apple Pay tokenization, but also offers multiple BIN options tailored to platforms like TikTok, Google, and AliExpress—ideal for ad buyers, e-commerce sellers, and SaaS users.

Step 1: Virtual Card Issuance Workflow

-

Card Request Submission Users apply for a virtual card via a frontend interface, specifying card type (single-use or reloadable), currency, spending limit, and intended platform.

-

Card Data Generation The system queries the BIN management engine and calls the processor to generate the card number, CVV, and expiration date, then binds the card to the user’s wallet.

-

Encryption & Storage Card details are encrypted and securely stored. Some platforms also support tokenization for Apple Pay or Google Pay integration.

Step 2: Authorization Flow

-

Initiate Payment When the card is used on platforms like Google, TikTok, or AliExpress, the payment request is routed via the card network to the issuer.

-

Real-Time Authorization The issuer's system performs several checks:

-

Is the card active and not expired?

-

Is the wallet balance sufficient?

-

Does the transaction pass fraud detection (country/IP/device rules)?

An authorization log is recorded, and the system responds with approval or denial.

📌 Note: Authorization is only a temporary hold. Actual funds are settled later during the clearing process.

Step 3: Clearing & Settlement

After authorization:

-

The merchant initiates clearing via the card network.

-

The issuer debits the user's wallet on the settlement date (usually T+1 or T+2).

-

User receives confirmation and updated balance details.

Core Modules in Virtual Card Architecture

| Module | Functionality |

| BIN Management System | Manages BIN routing, platform compatibility, and scheme mappings |

| Card Lifecycle System | Handles creation, activation, suspension, termination |

| Authorization Gateway | Real-time filtering, whitelisting, and rule-based risk checks |

| Clearing & Reconciliation | Tracks settlements, billing events, and payment network reconciliation |

| Risk Control Engine | Detects fraud, prevents duplicate transactions and chargebacks |

| Tokenization Module | Enables support for Apple Pay / Google Pay & secure, tokenized data transfers |

Key Benefits of Virtual Card Architecture

✅ Granular Control – Each card can have custom limits, use cases, and expiration dates

✅ Lower Risk Exposure – Platform-specific or one-time-use cards isolate threats

✅ Seamless Integration – API-based issuance and authorization workflows

✅ Higher Success Rates – Multi-BIN routing ensures better acceptance across platforms

Looking Ahead: On-Chain Virtual Cards & Smart Settlement

Emerging trends point to even smarter architectures:

🔗 On-Chain Settlement – Stablecoin-powered, T+0 real-time reconciliation

🤖 AI Risk Engines – Adaptive limit adjustments based on behavioral patterns

🧩 Modular Compliance Frameworks – Plug-and-play AML/KYC per jurisdiction or product line

Buvei’s clearing infrastructure already supports T+0 USDT settlements—tailored for ad platforms with frequent micro-transactions.

Final Thoughts

A robust virtual card architecture involves much more than just issuing numbers. From BIN optimization to real-time authorization and T+0 settlement, understanding the system behind the scenes is crucial for ad buyers, SaaS operators, and cross-border e-commerce players.

If you’re looking for a secure, multi-BIN, stablecoin-compatible virtual card platform with Apple Pay support and real-time risk controls, Buvei.com is one of the most capable solutions available.