In the payment industry, CPA (Cardholder Present Authorization) is a fundamental concept that plays a vital role in credit card transaction processing, risk management, and fund settlement. This article provides an in-depth look at CPA—its definition, operational mechanisms, and applications in the payment ecosystem.

What is CPA?

CPA refers to transactions where the cardholder is physically present and completes identity verification, typically used in POS terminals, ATM withdrawals, and in-store payments. In contrast, CNP (Card Not Present) transactions occur in e-commerce, phone orders, and other remote payment scenarios.

Key Features of CPA Transactions:

-

Enhanced Security – Since the cardholder must physically swipe, insert, or tap the card (e.g., EMV chip or NFC payments), fraud risk is significantly lower.

-

Lower Chargeback Rates – Banks and payment processors trust CPA transactions more due to physical card verification.

- Faster Settlement – Financial institutions often provide quicker fund clearance for CPA transactions, improving cash flow for merchants.

How CPA Impacts Payment Settlement & Reconciliation

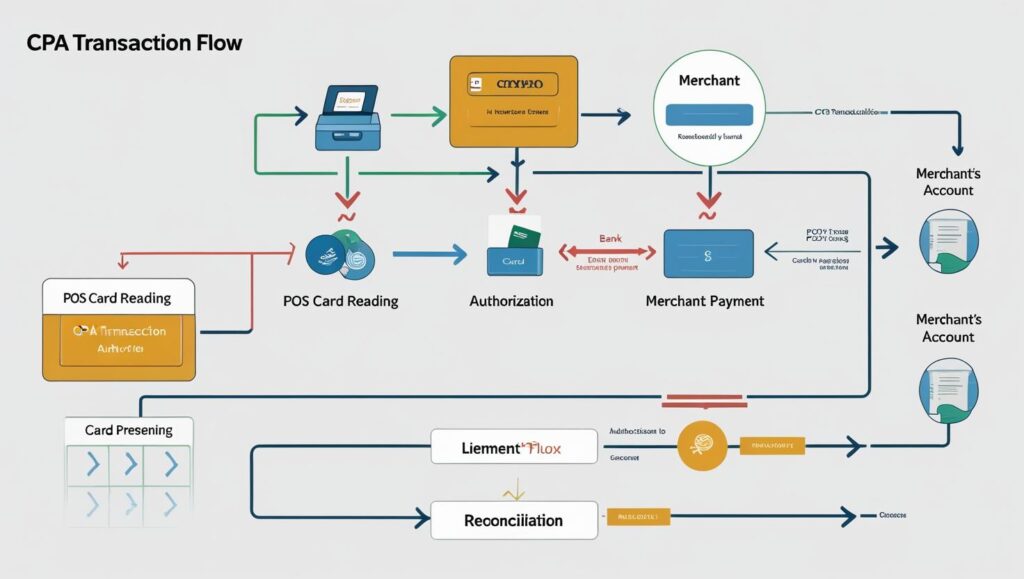

(1) Transaction Authorization Flow

When a customer pays via POS, the process follows these steps:

-

Card Presentment → The POS reads card details (card number, expiry date, etc.).

-

Risk Verification → The payment gateway (e.g., Buvei) requests authorization from the issuing bank.

-

Transaction Completion → If approved, funds are temporarily held and later settled to the merchant’s account.

(2) Fund Settlement & Reconciliation

-

T+1 or D+0 Settlement – CPA transactions often benefit from faster settlement cycles. Some providers even offer same-day settlement (D+0), optimizing cash flow for businesses.

-

Automated Reconciliation – Payment processors generate daily settlement reports, matching transaction records with actual bank deposits to minimize manual errors.

Case Study: Buvei’s Efficient Settlement Solution Buvei offers smart split settlements + T+0 funding for cross-border and retail merchants, enabling real-time CPA transaction clearing while reducing reconciliation costs—ideal for high-volume payment scenarios.

CPA & Fraud Prevention: Strengthening Payment Security

Since CPA requires physical card interaction, fraud rates are much lower than CNP transactions. Payment providers implement these security measures:

-

EMV Chip Technology – Prevents card cloning and enhances transaction security.

-

3DS Authentication (in select cases) – Some CPA transactions may integrate SMS/biometric verification.

-

Dynamic Transaction Limits – Providers like Buvei adjust risk controls for high-value CPA payments, balancing security and user experience.

The Future of CPA: Contactless Payments & Beyond

With the rise of NFC-based payments (Apple Pay, UnionPay QuickPass), CPA is evolving—even without physical card insertion, transactions with biometric verification (fingerprint/face ID) can still qualify as CPA. Payment providers must continuously refine risk models to adapt to new payment trends.

Final Thoughts

CPA remains a cornerstone of secure, efficient payment processing, directly influencing transaction approval rates, settlement speed, and merchant liquidity. Partnering with a smart payment provider like Buvei not only optimizes CPA transaction efficiency but also enhances financial operations through automated reconciliation and flexible settlement solutions.

Buvei Tip: If your business relies on in-person card payments, explore Buvei’s high authorization rates + instant settlement to streamline your cash flow!