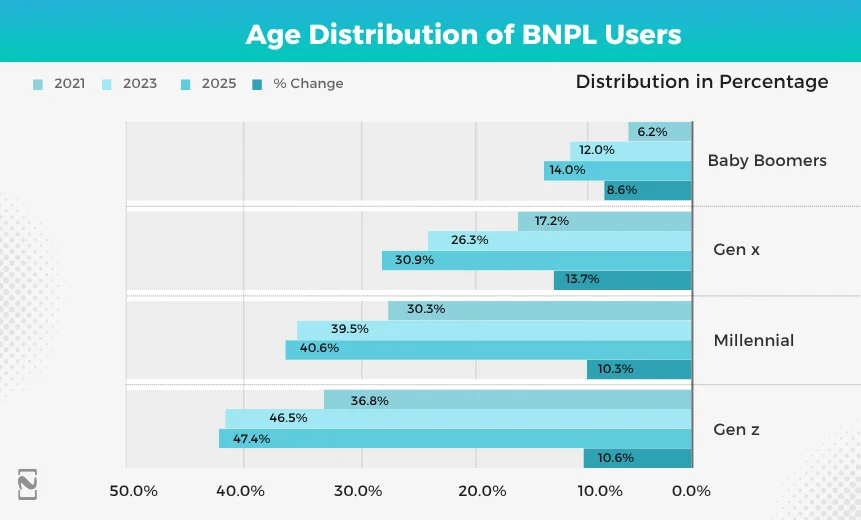

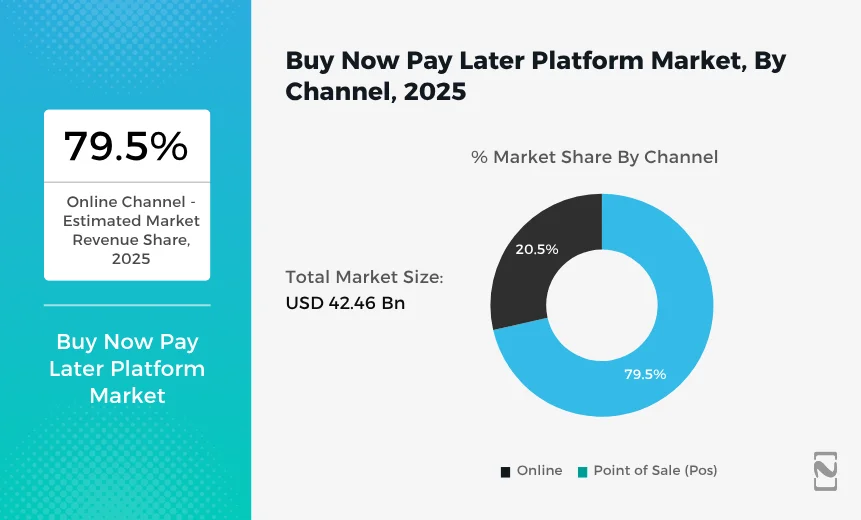

5Buy Now Pay Later (BNPL) is rapidly transforming the way consumers shop and merchants operate—particularly among Millennials and Gen Z. By 2025, the BNPL market is projected to reach $560.1 billion globally, growing at a CAGR of 13.7% (Fintech Futures, 2025).

What is BNPL?

BNPL enables consumers to split purchases into installments without having to pay the full amount upfront. Typically, the process involves:

-

A shopper selects BNPL at checkout (via Klarna, Afterpay, Affirm, or Apple Pay Later);

-

The BNPL provider pays the merchant in full;

-

The customer repays over time, often interest-free.

This flexible payment model improves affordability for consumers and boosts conversion rates and average order value (AOV) for merchants.

Market Trends & Regulatory Momentum

The global BNPL boom is being driven by the rise of e-commerce, mobile wallets, and digital-native consumers. Transaction volumes continue to surge across the US, UK, and Southeast Asia. Apple’s launch of Apple Pay Later has accelerated mainstream adoption.

However, regulatory bodies are responding quickly to the risks:

-

The UK and Australia are tightening credit assessment rules for BNPL providers (2024–2026 rollout);

-

The US CFPB plans to bring BNPL under the same rules as credit cards;

-

The EU’s upcoming PSD3 framework will mandate clearer fee disclosures and stronger consumer protections.

The message is clear: growth must be balanced with compliance and risk resilience.

The Hidden Risks Behind BNPL

Despite its user-friendliness, BNPL comes with several challenges:

-

Consumer Debt: 34% of BNPL users have missed payments, putting their credit scores at risk.

-

Fraud Exposure: Streamlined application processes attract malicious actors.

-

Merchant Liquidity: Platforms must pre-fund transactions, impacting cash flow.

-

Compliance Costs: Regulatory updates often require system overhauls.

As the market matures, risk management and compliance readiness are becoming strategic imperatives for BNPL players.

How Buvei Powers the Next Generation of BNPL

Buvei, an embedded payment infrastructure provider, offers full-stack solutions to address BNPL’s operational and compliance pain points.

-

🔐 AI-Powered Risk Intelligence

Buvei’s smart fraud detection engine leverages transaction patterns and on-chain data to assess user behavior in real-time—reducing fraud losses by up to 40% for partners. -

💱 Real-Time Settlement & Multi-Currency Support

With T+1 payouts and 30+ currencies supported, Buvei empowers BNPL providers to scale across borders without exchange rate frictions. -

⚖️ Compliance-Ready Architecture

Buvei’s modular APIs dynamically adjust to local regulations, covering everything from KYC/AML to fee disclosure in line with PSD3 and FCA guidelines.

What’s Next: BNPL Meets AI and Web3

BNPL is evolving beyond installment plans into smarter, decentralized credit models:

-

AI-Driven Credit Scoring

Personalized limits and real-time affordability assessments based on spending behavior and repayment history. -

Web3-Based BNPL

On-chain credit scores using DeFi lending histories, combined with stablecoin repayments, could unlock global, permissionless BNPL models.

Buvei is building the bridge between fiat and crypto through open APIs and blockchain-ready payment rails—fueling the next generation of credit innovation.