Digital fraud is evolving. The days of hackers simply stealing credentials and making unauthorized payments are giving way to a more complex threat: social engineering scams that trick users into authorizing fraudulent payments themselves.

According to recent reports, such as Cleafy’s Disrupting Digital Fraud guide, fraud now starts before the transaction is made. It begins with the first interaction between scammer and victim — where emotional manipulation and psychological tactics exploit human trust rather than technical vulnerabilities.

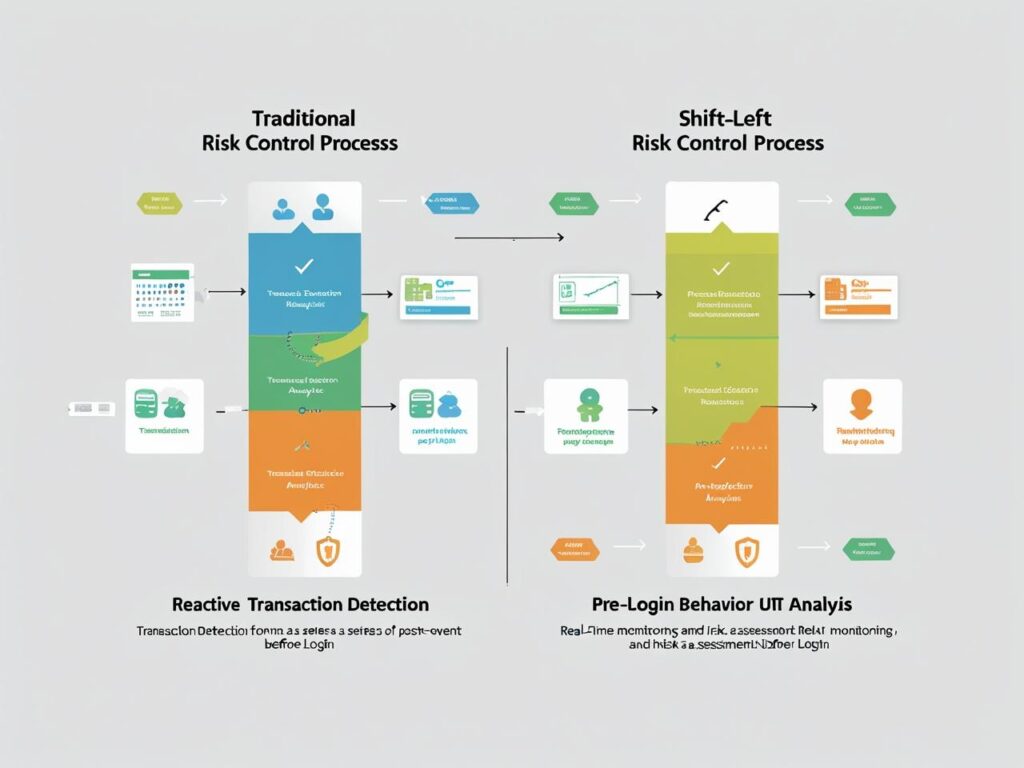

This shift challenges traditional fraud prevention, which often reacts to suspicious transactions after they occur. To effectively combat fraud today, financial institutions and businesses must detect suspicious behavior earlier in the customer journey — often called the ‘shift-left’ approach.

Why Early Fraud Detection is Critical: Hidden Costs and New Tactics

Cleafy’s report highlights that fraud is no longer just about lost money. It includes emotional harm, legal complexities, and the use of advanced technologies such as spoofed calls, fake websites, remote access tools, and deepfake media.

For example, in the UK, authorized push payment (APP) scams caused losses of £485 million in 2023, with many funds moved rapidly through “money mule” networks that help disguise stolen money.

Traditional fraud detection systems that focus solely on transaction anomalies miss the mark, as fraud starts well before the payment is submitted. Key early warning signs include:

-

Unexpected device or location changes during login

-

Remote access software activity

-

Unusual session behaviors like concurrent phone calls during payment

These signals require contextual, real-time behavioral analytics — moving from reactive detection to proactive prevention.

The Role of Money Mule Networks in Scaling Fraud

An often-overlooked aspect of digital fraud is the role of money mule accounts — individuals or synthetic identities that help fraudsters move and launder stolen funds.

These mules come in various forms:

-

Unwitting mules: Recruited unknowingly through fake jobs or remote offers

-

Witting mules: Those who knowingly rent out their accounts for a cut

-

Synthetic mules: Completely fake or hijacked identities created solely to move money

Detecting and dismantling these networks requires analyzing transactional flows beyond individual accounts and spotting suspicious patterns like large, irregular deposits followed by quick transfers.

Regulatory Trends Demand Smarter, Earlier Fraud Controls

Regulations such as PSD3, GDPR, the EU AI Act, and DORA are pushing financial institutions to adopt more transparent, proactive, and explainable fraud prevention measures.

-

PSD3 places liability on banks even for authorized scams, requiring them to prove due diligence

-

The EU AI Act demands explainability for AI-driven fraud detection models

-

DORA treats fraud resilience as a core operational risk, integrating it into tech infrastructure

This means fraud prevention solutions must be agile, compliant, and integrated deeply within operational workflows.

Buvei Virtual Cards: A Proactive Tool for Shift-Left Fraud Prevention

With this evolving fraud landscape, businesses need payment tools that provide early-stage risk mitigation, fine-grained control, and operational flexibility.

Buvei’s programmable virtual cards are designed precisely for this new paradigm:

-

Customizable Limits & Controls: Set spend caps, merchant whitelists, and usage restrictions to prevent unauthorized or suspicious charges before they happen

-

Single-Use & Merchant-Locked Cards: Issue one-time cards or tie cards to specific vendors, isolating risk and containing fraud impact

-

Real-Time Management: Instantly create, pause, or revoke cards to respond to emerging threats or anomalies

-

Compliance & Security: Buvei is PCI-DSS certified and supports regulatory demands for privacy and operational resilience

By embedding Buvei virtual cards into payment workflows, organizations add a critical layer of shift-left fraud prevention—stopping fraudulent activity at the authorization phase, before money leaves the account.

Use Cases: Where Buvei Virtual Cards Make a Difference

-

Digital Advertising Spend: Prevent ad fraud and unauthorized campaign charges by isolating spend per platform with dedicated cards

-

Subscription Services: Use merchant-locked cards for SaaS and recurring payments, limiting exposure if credentials are compromised

-

Cross-Border & Marketplace Payments: Control currency and region-specific risk through tailored card issuance

-

Employee Expense Management: Enforce spend policies and reduce fraud risk with per-employee virtual cards

These use cases align perfectly with Cleafy’s recommendations for behavioral monitoring combined with robust payment controls.

Fraud Prevention Starts Before the Payment

The future of fraud prevention lies in early detection and proactive disruption, not after-the-fact reimbursement.

Cleafy’s ‘shift-left’ strategy underscores that detecting suspicious behavior and intervening early is essential to protect users and businesses alike. Buvei virtual cards offer a practical, effective solution to operationalize this approach, delivering programmable, secure payment instruments that reduce risk and improve user experience.

For organizations seeking to stay ahead of evolving fraud threats, integrating Buvei’s virtual cards into their fraud prevention arsenal is a critical step toward safer, smarter payments.

👉 Learn more about Buvei’s virtual cards and how they support advanced fraud prevention: https://buvei.com