Launching a branded payment program has become significantly easier with the rise of embedded finance. However, understanding the true white-label virtual card issuing cost is essential before committing to any provider.

In 2026, pricing varies widely across platforms due to differences in regulatory coverage, infrastructure, funding methods, and service levels. What appears inexpensive upfront may become costly once transaction fees, compliance expenses, and operational charges are included.

How White-Label Virtual Card Pricing Works

White-label virtual card providers typically use multi-layered pricing models rather than a single subscription fee. Costs are distributed across setup, issuance, funding, transactions, and ongoing management.

Because these programs rely on licensed banks and card networks, pricing reflects not only payment processing but also regulatory compliance, fraud monitoring, and technical infrastructure.

Common pricing approaches include:

-

Pay-per-transaction fees

-

Monthly platform subscriptions

-

Revenue-sharing agreements

-

Volume-based discounts

-

Hybrid pricing structures

Programs designed for customer distribution often cost more than internal corporate expense solutions due to additional compliance requirements.

Common Fees in Card Issuing Platforms

Businesses evaluating providers should review fee schedules carefully. The most significant expenses typically fall into several categories.

Setup and Onboarding Fees

Some providers charge initial fees to configure the program, perform compliance checks, and establish issuing arrangements. These are more common in fully regulated banking partnerships.

Card Issuance Fees

Each virtual card generated may carry a small charge, particularly when issued in large volumes or across multiple regions.

Transaction Processing Fees

Every payment processed through the card network can incur a percentage-based or fixed fee. Cross-border transactions often cost more.

Funding Fees

Transferring funds into the card system — especially via international bank wires — may involve intermediary banking charges and currency conversion costs.

Platform or Maintenance Fees

Recurring monthly charges may cover dashboard access, reporting tools, and operational support.

Foreign Exchange Costs

Programs involving multi-currency transactions often include FX spreads that can materially affect total spending.

Even small fees can accumulate quickly at scale, making transparency a key factor in provider selection.

Factors That Affect Virtual Card Issing Costs

Several variables determine the overall cost of a white-label program.

Transaction Volume

Higher usage typically leads to better pricing tiers. Low-volume programs often pay higher per-transaction fees.

Geographic Scope

Issuing cards for use across multiple countries requires additional regulatory coordination and network agreements, increasing operational costs.

BIN Region

Cards issued under certain regions — particularly those with high approval rates — may involve different pricing structures.

Funding Method

Traditional banking channels can be slow and expensive for international transfers. Alternative funding mechanisms may reduce both cost and settlement time.

Compliance Requirements

Programs targeting regulated industries or consumer markets generally require more extensive monitoring and reporting.

How Businesses Optimize Card Issing Costs

Organizations can significantly reduce expenses through careful program design.

Consolidate Payment Flows

Minimizing the number of transfers into the system reduces banking and conversion fees.

Use Spend Controls Strategically

Setting limits per card prevents overspending and simplifies reconciliation.

Scale Gradually

Negotiating volume discounts becomes easier once transaction levels increase.

Monitor Real-Time Data

Access to detailed transaction reporting allows businesses to identify inefficiencies early.

Evaluate Alternative Funding Options

Companies operating globally increasingly explore digital asset funding to reduce cross-border friction.

Using Buvei for Cost-Effective Card Issuing

Among modern platforms, Buvei is often considered by businesses seeking a cost-efficient approach to global virtual card deployment, particularly for online payments and digital services.

Stablecoin Funding to Lower Transfer Costs

Accounts can be funded using USDT on TRC20 or ERC20 networks, which may reduce international transfer fees and accelerate settlement compared with traditional bank wires.

Multi-BIN Support for Better Payment Efficiency

Access to multiple BIN regions allows businesses to select cards that perform reliably with target merchants, reducing failed transactions and associated operational costs.

Instant Virtual Card Issuance

Cards can be generated shortly after funding, eliminating delays associated with physical production and shipping.

Transparent Pricing Visibility

Fees related to funding and transactions are displayed within the dashboard, enabling clearer budgeting and forecasting.

Centralized Multi-Card Management

A single account can issue and manage numerous cards, helping organizations allocate budgets across teams or projects efficiently.

How to Create a Virtual Card with Buvei (Step-by-Step)

For businesses evaluating practical implementation, the onboarding process is straightforward.

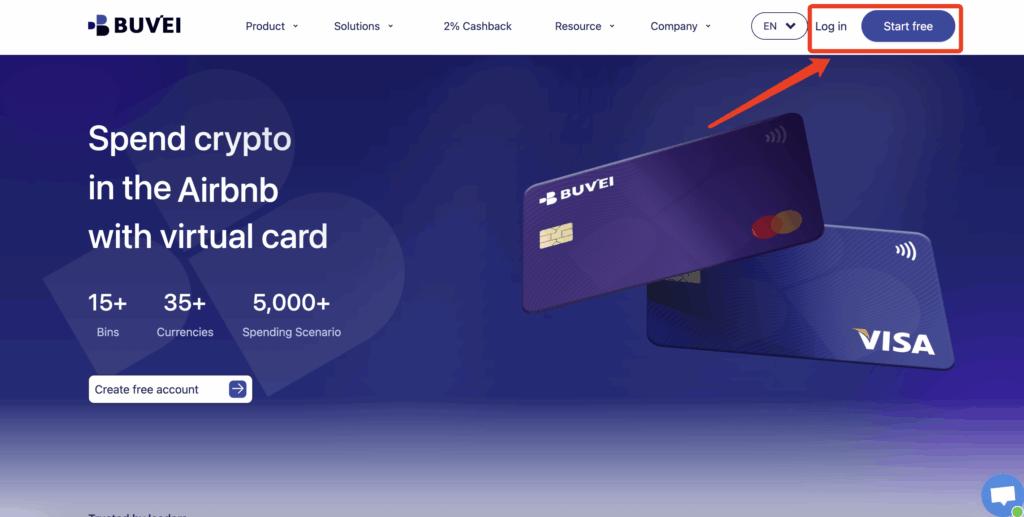

Step 1: Register a Buvei Account

Visit https://buvei.com

Create a free account and complete email verification. After verification, log in to access the Buvei dashboard.

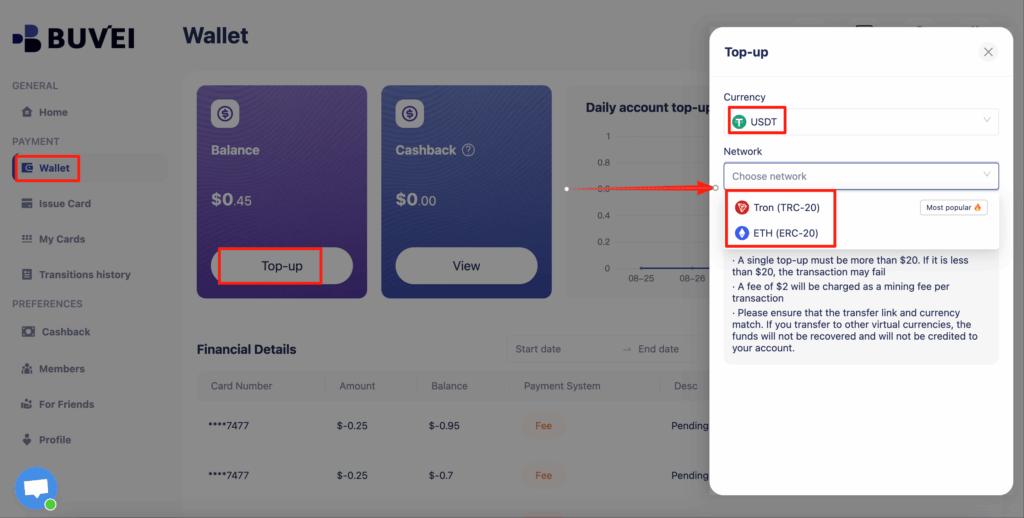

Step 2 — Fund Your Wallet

Navigate to the Wallet tab and deposit supported stablecoins such as USDT.

-

Choose TRC20 or ERC20 network

-

Copy your unique deposit address

-

Transfer funds from a crypto wallet or exchange

-

After confirmation, the balance appears in your wallet

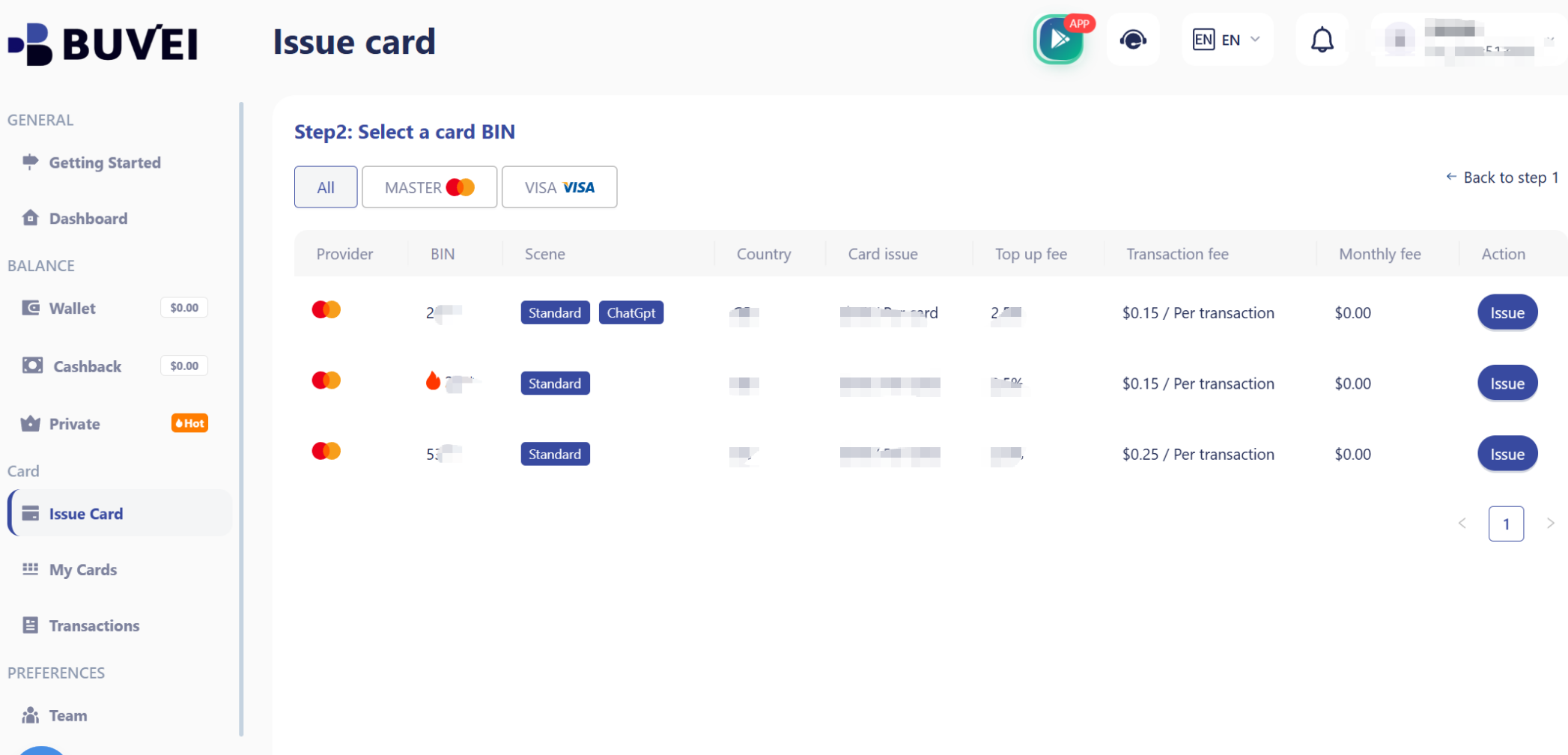

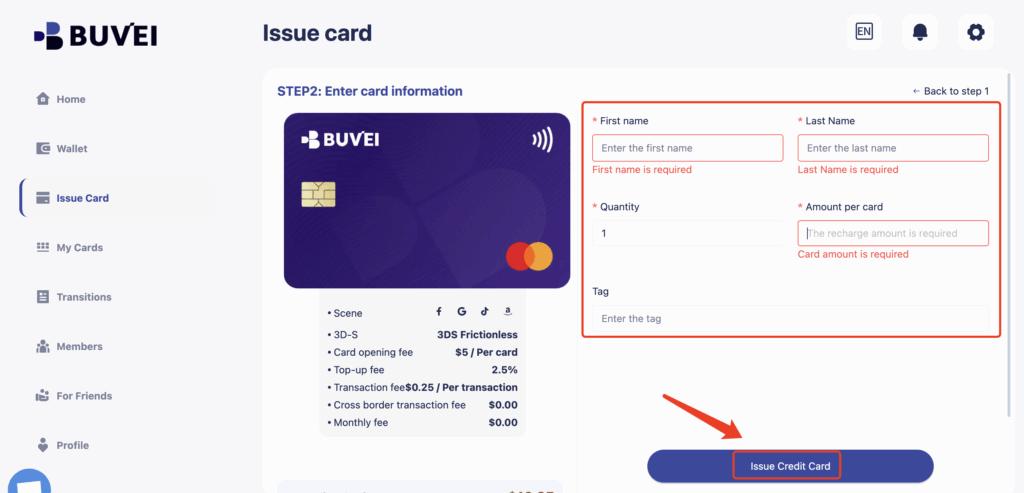

Step 3 — Create a Virtual Card

Go to the Cards section.

Select your preferred BIN region (U.S. BIN commonly recommended)

Choose card type

Enter card details — name, funding amount, and quantity

Click Issue Card

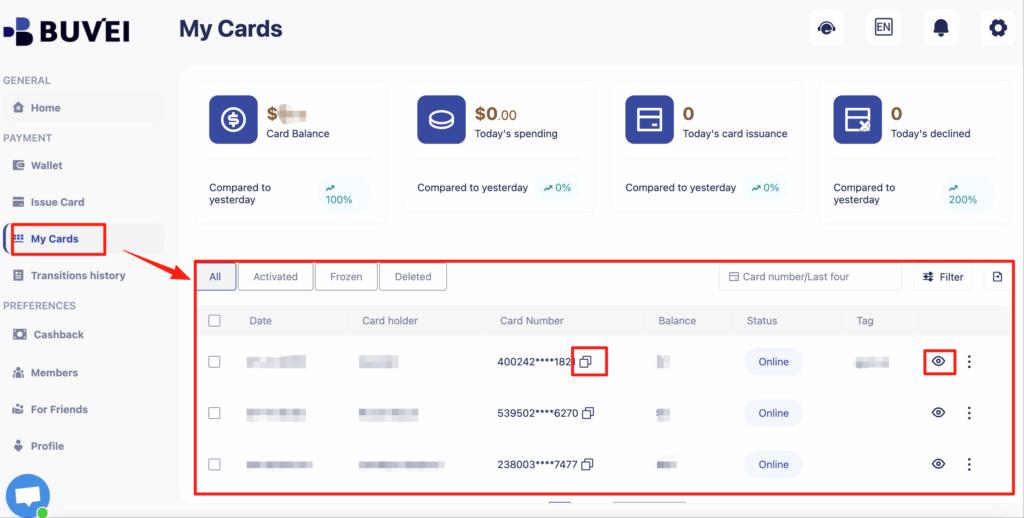

Step 4 — Access Card Details

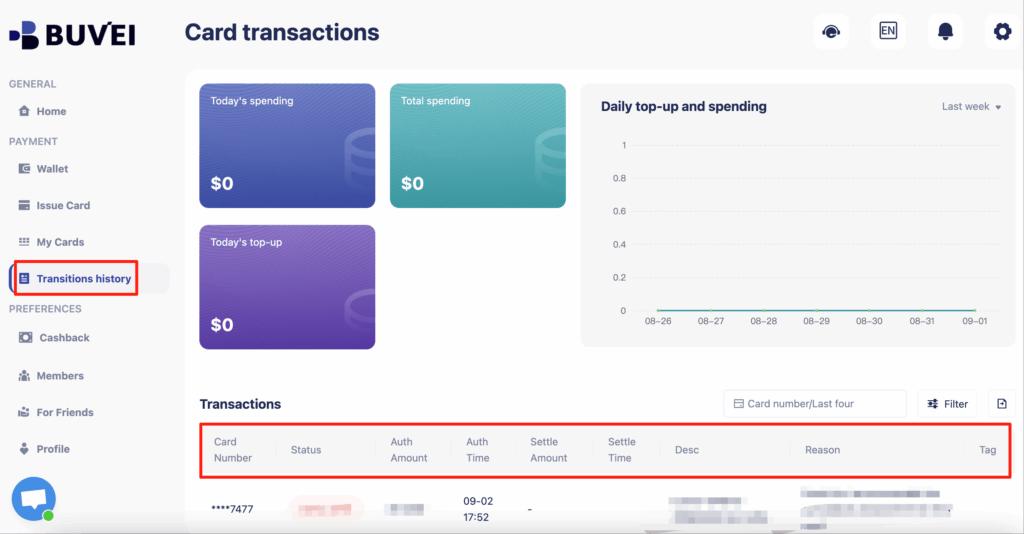

Under My Cards, you can view:

-

Card number

-

Expiration date

-

CVV

-

Balance and transaction history

The card can then be used immediately for online payments, subscriptions, or operational expenses.

Final Thoughts

Understanding the white-label virtual card issuing cost is critical for building a sustainable payment program. While pricing models vary across providers, total expenses depend on transaction volume, geographic coverage, funding methods, and compliance requirements.

Businesses that prioritize transparency, flexible funding, and operational efficiency tend to achieve the lowest long-term costs. For organizations seeking a streamlined approach to global digital payments, platforms such as Buvei offer a practical solution for issuing and managing virtual cards without the overhead associated with traditional banking infrastructure.