As digital transactions become more common, so do the risks associated with them. In the face of phishing scams, credential theft, and account takeovers, Two-Factor Authentication (2FA) has emerged as one of the most effective methods to secure user accounts and financial operations.

But what exactly is 2FA, and why is it considered a must-have in today’s payment infrastructure?

What Is Two-Factor Authentication (2FA)?

2FA is a security process that requires users to provide two different types of authentication factors to verify their identity. It typically combines:

-

Something you know – e.g., a password or PIN

-

Something you have – e.g., a smartphone, a hardware token, or an authentication app

-

(Optional) Something you are – e.g., biometric data like fingerprints or facial recognition

This layered approach makes it significantly harder for unauthorized users to access sensitive accounts, even if they’ve managed to steal a password.

Why 2FA Matters in the Payment Industry

In the context of financial transactions, the stakes are much higher. Here’s why 2FA is no longer optional:

-

🔐 Prevents Unauthorized Access to Payment Accounts

Payment platforms are prime targets for cybercriminals. With 2FA in place, even stolen login credentials are insufficient for unauthorized access—protecting virtual card accounts, digital wallets, and payment dashboards.

-

🛡 Meets Compliance and Regulatory Requirements

Financial institutions and fintech platforms are increasingly required to implement multi-factor authentication to meet local and global standards such as PSD2 (EU), PCI DSS, and FFIEC (US).

-

🧠 Reduces Human Error & Social Engineering Risk

Even tech-savvy users can fall for phishing attempts. By requiring a second factor (e.g., a code from an app like Google Authenticator or a hardware key), platforms can neutralize most credential stuffing or impersonation attacks.

-

📲 Secures Mobile and API-Based Payments

With mobile-first usage dominating the payment space, 2FA adds a critical layer of security to app logins, API token authorizations, and even biometric-triggered payments.

-

💳 Protects Virtual Card Operations

For platforms like Buvei that offer virtual cards, 2FA can be tied to the card issuance, modification, or fund recharging process—mitigating the risk of internal fraud or external exploitation.

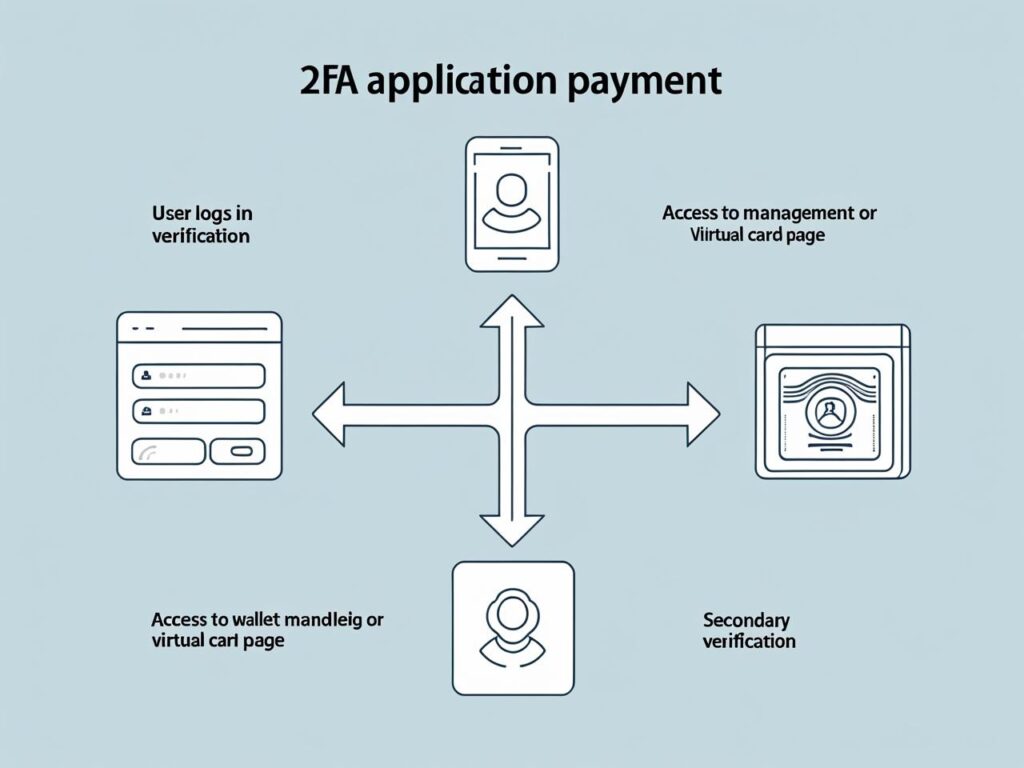

2FA in Action: Use Cases for Payment Platforms

-

🔁 Login Protection – Secure user logins from different IPs or devices

-

💼 Admin Panel Access – Enforce 2FA for employees managing finance or compliance

-

💰 Transaction Approval – Require 2FA for fund transfers, card top-ups, or API access

-

🧾 Subscription Management – Authenticate recurring payments or plan upgrades

Implementing 2FA: Best Practices for Fintechs and Merchants

-

Enable TOTP-based authentication via apps like Google Authenticator or Authy

-

Allow users to activate SMS or email backup codes (with security warnings)

-

Support WebAuthn / hardware tokens (e.g., YubiKey) for enterprise-grade protection

-

Implement risk-based triggers (e.g., device change or geo-location anomaly)

-

Provide clear, user-friendly 2FA setup instructions during onboarding

Security Without Friction

2FA balances usability and protection—making it one of the most cost-effective ways to secure payment operations. As digital finance continues to evolve, platforms that don’t implement 2FA are not just risking their users, but also their brand, revenue, and regulatory standing.

At Buvei, 2FA is a fundamental part of how we protect our virtual card users, API clients, and partners. Whether you're a business scaling payment flows or an individual managing ad spend, enabling 2FA is no longer a suggestion—it's a standard.

Frequently Asked Questions (FAQ)

Q1: Is 2FA required for all payment platforms?

Not all platforms require 2FA by default, but most compliant fintechs and licensed institutions do. In many jurisdictions, regulations like PSD2 mandate strong customer authentication.

Q2: What’s the difference between 2FA and MFA?

2FA refers to two authentication factors. MFA (Multi-Factor Authentication) refers to two or more. All 2FA is MFA, but not all MFA is just two factors.

Q3: What if I lose access to my 2FA device?

Most platforms (including Buvei) offer backup methods such as recovery codes, email verification, or account reset via KYC-based identity verification.

Q4: Can hackers bypass 2FA?

While no system is 100% secure, 2FA significantly reduces attack success rates. Sophisticated phishing and SIM-swap attacks exist, but combining TOTP + device alerts mitigates most threats.

📌 Need a secure virtual card with built-in 2FA controls?

Explore Buvei’s secure payment solutions and take control of your payment security.