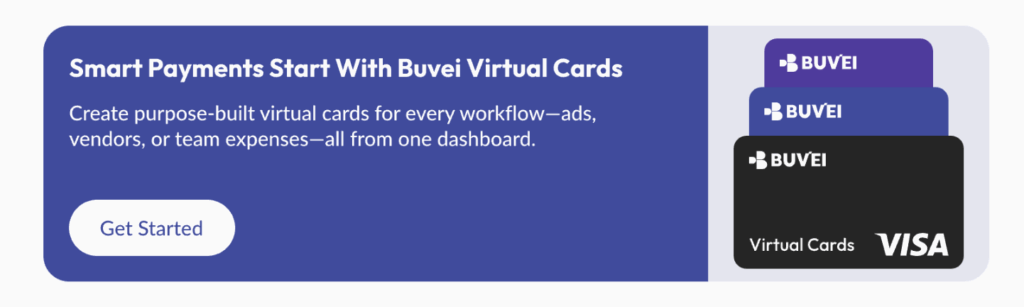

In today’s increasingly digital world, the need for flexible and secure payment methods is more pressing than ever—especially in Egypt. Whether you are a freelancer receiving international payments, an online shopper paying in USD, or simply looking for an alternative to traditional banking, a virtual card offers a compelling solution. In Egypt, traditional cards often face restrictions for foreign-currency transactions or international payments, making alternatives more attractive. This article outlines how to get a virtual card in Egypt, discusses four key strategies for making it happen, and gives you actionable tips to enhance credibility and trust in your payment solution.

Understand why you need a virtual card in Egypt

-

Many Egyptian debit or credit cards struggle with international payments, either because of foreign‐currency restrictions or high conversion fees.

-

A virtual card allows you to transact online globally, often in USD or other currencies, without waiting for physical card issuance.

-

It adds extra security: since it’s digital, you can often freeze or cancel it quickly if needed, reducing fraud risk.

-

For freelancers, exporters or digital nomads based in Egypt, a virtual card can be the gateway to global e-commerce, subscription services or payments that require international acceptance.

Strategy for credibility: When discussing this need, cite local data or banking-policy references (for example from the Central Bank of Egypt) about foreign-currency card restrictions. This reinforces your authority.

Choose the right provider and verify eligibility

-

Research virtual-card providers that support Egyptian residents. For example, providers such as Grey (virtual USD Mastercard) allow Egyptians to apply, fund a foreign-currency account and get the card.

-

Also check Egyptian-based fintech solutions: for example the Paysky Yalla app offers issuance of prepaid and virtual cards for individuals in Egypt.

-

Determine the required documentation: many services demand a government-issued ID, proof of address and KYC verification. Grey, for instance, describes this step clearly.

-

Confirm the currency, fees, reload options (bank transfer, USDT, etc), and whether you’ll need to open a foreign-currency account first.

Strategy for credibility: Provide a comparative table of at least two providers (local vs international), and show data such as fees, currencies supported, and user testimonial quotes (if available). This adds depth and trustworthiness.

Step-by-step process to get the virtual card

Here is a typical procedure you can follow, adapted for Egypt:

-

Step 1: Sign up for the service by downloading the provider’s app or visiting their website. Upload your identity documents, complete the KYC verification. (Example: Grey’s sign-up and verification process)

-

Step 2: Fund the account or foreign-currency wallet as required. For instance, with Grey you request a foreign currency (USD) account and then load it.

-

Step 3: Apply for the virtual card. Often you’ll be able to generate the card instantly inside the app, choose the spending limit or currency. For example, with American Express virtual cards in Egypt you log in to their app and navigate to “Virtual Cards Management”.

-

Step 4: Use your virtual card for online transactions. Add it to digital wallets if supported. Monitor usage, set controls and ensure you understand reload or expiry terms.

Strategy for credibility: Include a checklist the reader can tick off when following these steps. Also mention potential pitfalls (for example: card declines due to geolocation blocking, unsupported currency, or insufficient funds).

Security, compliance and best practices

-

Ensure the provider complies with payment industry standards (e.g., PCI DSS) and that your data is protected.

-

Set spending limits and monitor your transactions regularly. Virtual cards often allow you to freeze them or generate a new number in case of suspected misuse.

-

Keep in mind local regulatory limitations in Egypt: for instance, foreign-currency usage and cross-border transactions may be subject to oversight by the Central Bank of Egypt.

-

Keep your personal bank and virtual‐card credentials separate. Use strong passwords, enable multi-factor authentication and avoid public Wi-Fi when making financial transactions.

-

For SEO credibility: cite recent date references, show you researched local market conditions (Egypt), and mention both consumer and business use-cases.

Strategy for credibility: Add a short FAQ section with real questions Egyptians might ask (e.g., “Will an Egyptian-issued virtual card work on Netflix US?”, or “What happens if my local bank blocks foreign transactions?”). Provide concise answers.

Conclusion

As Egypt's digital economy expands and more users transact internationally, the adoption of virtual cards becomes a practical and strategic tool. By understanding why you need one, selecting the right provider, following a clear process, and maintaining good security practices, you can unlock global payments from Egypt with ease. Whether you're a freelancer, an online shopper, or someone looking for flexible payment options, a virtual card offers convenience, control and security. By applying the steps and strategies outlined above, you’ll be well-positioned to navigate the path confidently and credibly.