As the digital economy accelerates, payment technologies continue to evolve. Among the most powerful tools reshaping financial control and risk management are virtual cards and single-use cards. While both are designed to enhance security and streamline corporate spending, they serve different purposes.

This article explains their key differences, best use cases, and how platforms like Buvei optimize both types to meet modern business needs.

What Is a Virtual Card?

A virtual card is a digitally issued payment card that functions like a traditional credit or debit card. Issued by banks or fintech platforms, it comes with a 16-digit card number, expiration date, and CVV—just like a physical card—but exists only in digital form and is typically tied to a funding source or budget.

Virtual cards are reusable and can be configured with rules for:

-

Recurring subscription payments

-

Departmental or employee spending

-

Advertising budgets (e.g., Google, Meta)

-

B2B supplier payments

Platforms such as Buvei, Ramp, allow businesses to instantly generate multiple virtual cards with custom permissions—like spend limits, expiration dates, or merchant restrictions.

What Is a Single-Use Card?

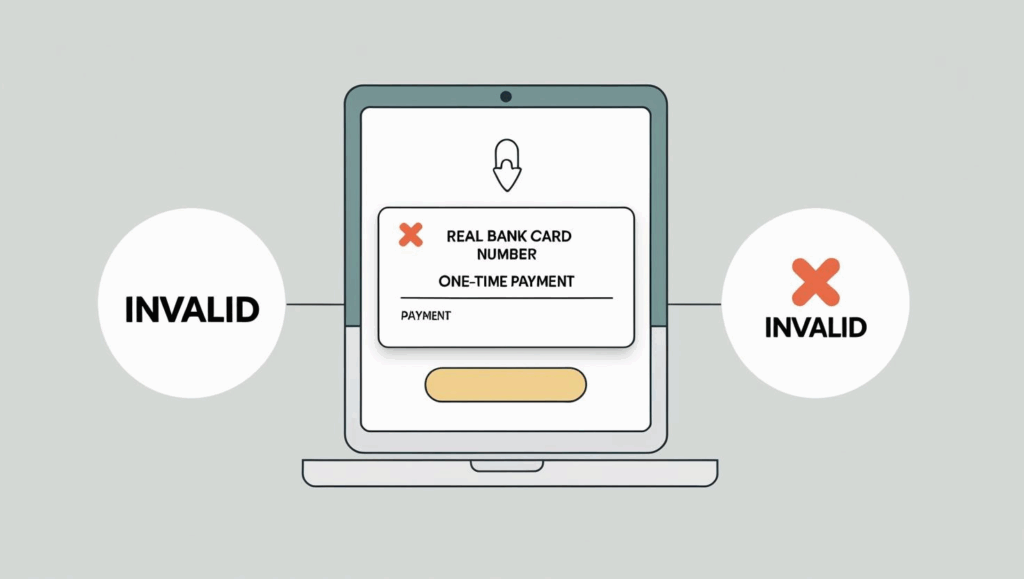

A single-use card (also known as a disposable card) is a subtype of virtual card designed for one-time use. It becomes invalid immediately after its first transaction, making it ideal for minimizing fraud risks.

Common use cases include:

-

Payments to new or untrusted vendors

-

Online bookings (hotels, flights, etc.)

-

Payouts to temporary contractors or consultants

-

Trial-period subscriptions

Platforms like American Express Go, Divvy, and Emburse offer single-use cards to reduce unauthorized charges and increase transaction security.

Side-by-Side Comparison

| Feature | Virtual Card | Single-Use Card |

| Usage Frequency | Reusable | One-time only |

| Security | High | Very high |

| Best for | Subscriptions, recurring business expenses | One-off purchases, unknown merchants |

| Validity Period | Days to years | Expires after use |

| Control Options | Customizable rules and limits | Fixed limit, auto-expiry |

Which One Is Right for You?

Choose a virtual card if you:

-

Make regular subscription or ad payments

-

Need to manage team budgets or internal spending

-

Want both flexibility and control over funds

Choose a single-use card if you:

-

Are transacting with an unfamiliar or untrusted vendor

-

Want to reduce the risk of card data compromise

-

Need a temporary payment method for contractors or guests

Buvei Advantage: Flexibility Meets Security

With Buvei, you can manage both virtual and single-use cards under a single platform:

-

Instantly issue reusable virtual cards for ad accounts, payroll, or procurement

-

Support for major stablecoins like USDT (TRC20/ERC20)

-

Powerful control features: set limits, merchant lock, real-time transaction tracking, or terminate a card instantly

Frequently Asked Questions

Q: Can I use a single-use card for subscriptions?

A: No. Single-use cards expire after the first payment and are not suitable for recurring billing.

Q: Where can virtual cards be used?

A: Anywhere that accepts Visa, Mastercard, or Amex—including most online and SaaS merchants.

Q: How fast do single-use cards expire?

A: Immediately after their first use, or automatically within minutes/hours if unused.

Final Thoughts

Both virtual and single-use cards are designed to make business payments safer and more efficient. By using them strategically, companies can align payment methods with specific workflows, reduce fraud risks, and improve financial visibility.

Ready to issue secure, enterprise-grade virtual cards?

Sign up for free at Buvei.com and start streamlining your global payment operations today.