Paper checks have been part of the financial system for decades.

However, in a digital-first economy, they are becoming increasingly difficult to justify.

In 2025, the U.S. federal government signaled a major shift by announcing that paper checks will no longer be the default for federal payments. This move isn’t symbolic. It reflects a broader reality: paper checks are slow, expensive, and risky—and businesses that continue relying on them are falling behind.

Why Paper Checks No Longer Make Sense

At first glance, paper checks may feel familiar and reliable. In practice, they introduce unnecessary friction.

Higher Cost, Lower Efficiency

Paper checks require:

-

Printing and mailing

-

Manual processing

-

Reconciliation and exception handling

These steps add up. Supporting check-based payments costs organizations millions each year in labor, infrastructure, and delay.

Increased Fraud and Security Risk

According to U.S. Treasury data, paper checks are far more likely to be:

-

Lost

-

Stolen

-

Altered

Compared to digital payments, checks expose businesses to significantly higher fraud risk.

Slow Settlement and Poor Visibility

Checks move at human speed, not system speed.

This creates:

-

Cash flow delays

-

Limited real-time visibility

-

Inaccurate forecasting

For finance teams, that lack of clarity is a real operational risk.

Why Businesses Still Use Paper Checks

If checks are so inefficient, why do they persist?

Process Inertia

Many organizations stick with checks because:

-

“That’s how it’s always been done”

-

Systems feel too complex to change

-

Vendors still accept checks

Unfortunately, this inertia compounds risk over time.

Fragmented Payment Workflows

In industries like construction, real estate, and professional services, payments often involve:

-

Multiple parties

-

Approval layers

-

Compliance requirements

Checks appear simple—but they actually make coordination harder.

How Digital Payments Change the Equation

Digital payments are not just faster. They fundamentally improve how money moves.

Built-In Audit Trails

Digital payments create:

-

Automatic records

-

Clear transaction histories

-

Easier compliance reporting

This reduces errors and simplifies audits.

Faster Access to Capital

When payments settle quickly:

-

Vendors get paid sooner

-

Cash flow improves

-

Working capital is freed

Speed becomes a competitive advantage.

Stronger Controls and Transparency

Modern payment systems allow:

-

Spending limits

-

Approval rules

-

Real-time monitoring

This gives CFOs and finance teams better control over risk.

Digital Payments as a Strategic Advantage

More companies are realizing that payments are not just a back-office task.

In complex sectors, digital payment platforms now:

-

Coordinate multi-party transactions

-

Reduce disputes

-

Accelerate project timelines

What used to be an operational burden is becoming a strategic lever.

Moving From Checks to Modern Payment Tools

For businesses ready to move away from checks, the transition doesn’t have to be disruptive.

One Practical Option: Virtual Card Payments

Virtual cards allow businesses to:

-

Pay vendors digitally

-

Control spending per transaction

-

Eliminate paper-based workflows

They are especially useful for recurring or controlled payments.

Example: Using Buvei for Digital Business Payments

Buvei offers virtual card infrastructure that helps businesses replace manual payment methods.

Step 1: Create a Buvei Account

-

Visit https://buvei.com

-

Register a free account and verify your email

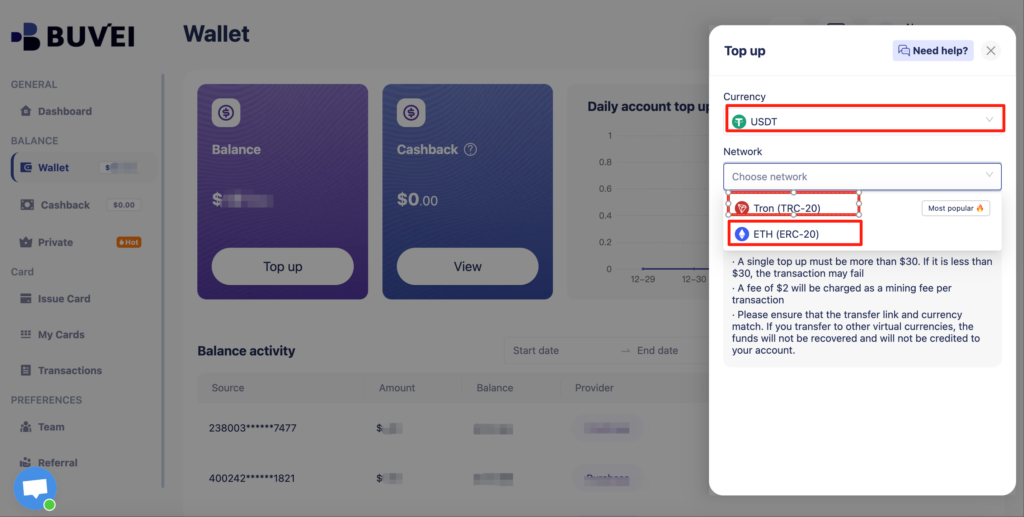

Step 2: Fund Your Wallet

-

Add funds using USDT (TRC20 or ERC20)

-

Funds are available once confirmed

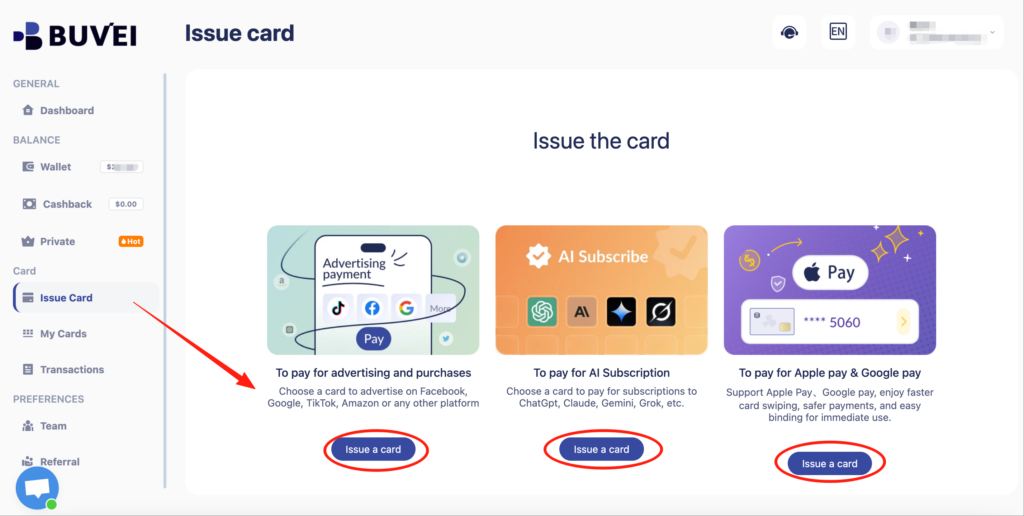

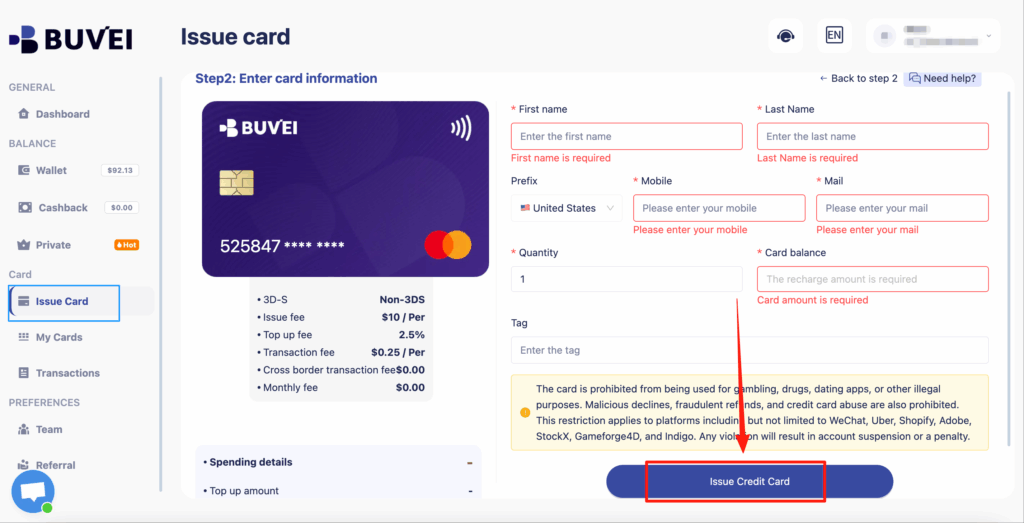

Step 3: Issue Virtual Cards

-

Create reusable virtual cards

-

Set limits and track transactions in real time

This approach removes the delays and risks associated with paper checks while maintaining control and visibility.

Final Thoughts

Paper checks are no longer a sign of reliability. They’re a sign of inefficiency.

As the federal government moves away from checks, the private sector faces a clear choice:

-

Continue absorbing unnecessary risk and cost

-

Or adopt digital payment systems built for today’s economy

Digitizing payments isn’t just modernization.

It’s about security, resilience, and operational clarity—and the businesses that act now will be better positioned for what comes next.