Card issuing APIs have become a core component of modern payment infrastructure. Businesses today—from SaaS platforms to fintech startups—use APIs to create virtual cards instantly, automate billing workflows, and manage global payments at scale.

1. What Is a Card Issuing API

A card issuing API is a software interface that allows businesses to create and manage payment cards programmatically.

Instead of manually requesting cards from banks, companies can generate virtual cards automatically through code.

Simple Definition

A card issuing API enables businesses to:

Create virtual cards instantly

Set spending limits

Assign cards to users

Track transactions

Control payment permissions

These APIs are commonly provided by financial infrastructure companies such as Stripe, Marqeta, and Adyen.

Why Card Issuing APIs Matter in 2026

Modern businesses operate across multiple regions, currencies, and platforms. Manual payment processes are no longer practical.

Card issuing APIs help businesses:

Automate financial operations

Improve payment approval rates

Reduce operational overhead

Scale globally

Improve expense visibility

These capabilities are especially valuable for fast-growing digital businesses.

2. How Card Issuing APIs Work Step by Step

Behind every virtual card is a structured workflow involving multiple payment components.

Here is a simplified step-by-step overview.

Step 1: Business Connects to the API

A company integrates its internal system with a card issuing platform.

This typically involves:

Creating developer credentials

Setting API authentication keys

Connecting backend systems

Once integrated, the system can request card creation automatically.

Step 2: Card Request Is Sent

When a new card is needed, the system sends a request to the API.

Typical request parameters include:

Cardholder ID

Spending limit

Currency

Expiration settings

Merchant restrictions

This step determines how the card will behave.

Step 3: Card Is Generated Instantly

The issuing platform generates a virtual card using available card infrastructure.

This includes:

Card number

Expiration date

CVV code

Billing configuration

The card becomes available within seconds.

Step 4: Card Is Used for Payments

The virtual card can be used immediately for online transactions.

Common payment destinations include:

Google advertising accounts

Meta Platforms campaigns

Amazon services

Subscription tools

Payments are processed through standard card networks.

Step 5: Transaction Data Is Returned

After each transaction, the API sends detailed data back to the business.

This includes:

Transaction amount

Merchant details

Payment status

Decline reasons

Businesses use this data for reporting and automation.

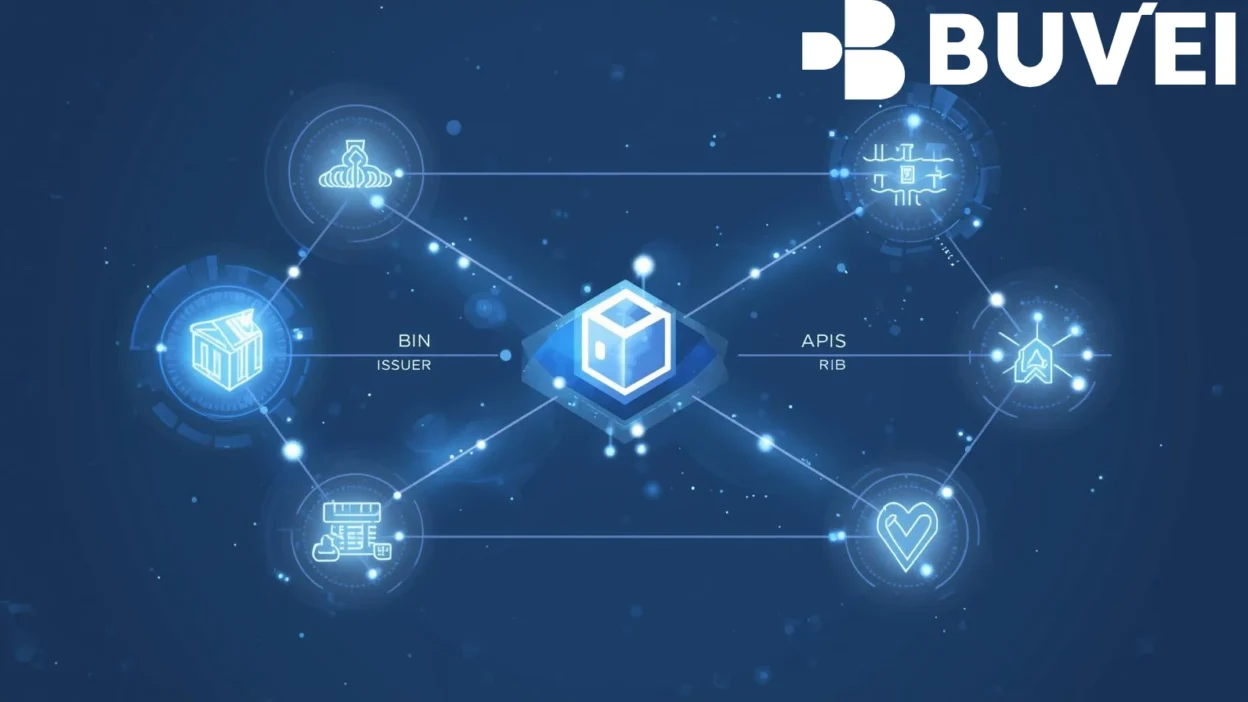

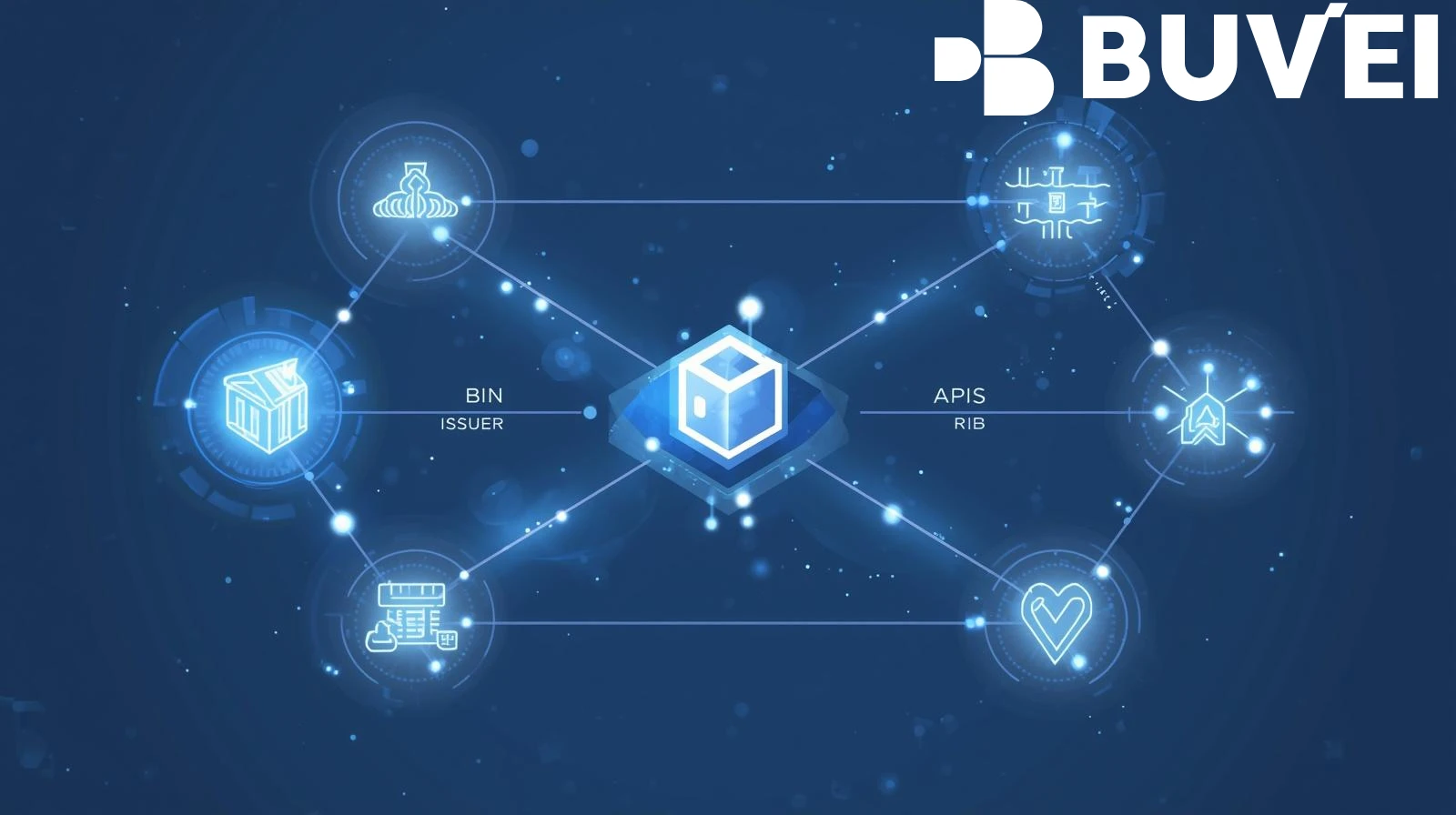

3. Key Components: BIN, Issuer, Processor, API

Several technical elements work together to make card issuing possible.

Understanding these components helps clarify how the system functions.

BIN (Bank Identification Number)

A BIN is the first six to eight digits of a payment card.

It identifies:

Issuing bank

Card type

Geographic region

Payment network

BIN quality affects:

Payment approval rates

Merchant compatibility

Geographic acceptance

Multiple BIN options improve payment reliability.

Issuer Bank

The issuer is the financial institution responsible for creating and managing the card.

Issuer banks:

Approve transactions

Monitor fraud

Manage compliance

Hold financial liability

Without an issuer, cards cannot function.

Payment Processor

Processors handle communication between merchants and issuing banks.

They manage:

Authorization requests

Transaction routing

Settlement processes

Payment confirmation

Reliable processors reduce payment failures.

Card Issuing API Platform

The API platform connects all components together.

It provides:

Developer tools

Card management systems

Transaction dashboards

Security frameworks

This is the interface businesses use to control payment workflows.

4. Use Cases: SaaS, Ads, Fintech Platforms

Card issuing APIs support a wide range of industries.

Below are the most common real-world applications.

SaaS Billing and Subscription Management

Software companies frequently rely on recurring billing.

Virtual cards help:

Pay for cloud services

Manage subscription tools

Track departmental spending

Control recurring charges

These features simplify subscription management.

Advertising and Media Buying

Marketing teams often run multiple campaigns simultaneously.

Virtual cards allow:

Separate campaign budgets

Controlled ad spend

Fast payment approvals

Real-time cost tracking

Platforms commonly supported include:

Google Ads

Meta Ads

TikTok

Campaign-level card control improves financial efficiency.

Fintech and Embedded Finance Products

Many fintech platforms build services on top of issuing APIs.

Examples include:

Digital wallets

Expense tracking apps

Corporate card programs

Payment automation tools

Embedded finance relies heavily on API-driven infrastructure.

Marketplace and Platform Payments

Online marketplaces use virtual cards to manage payments between parties.

Common functions include:

Vendor payouts

Refund handling

Transaction tracking

Budget segmentation

These systems reduce manual payment errors.

5. How buvei Provides Card Issuing API Solutions

Modern card issuing platforms provide infrastructure designed for automation-heavy businesses.

Flexible API Integration

API issuing platforms typically support:

Instant card creation

Custom spending rules

Real-time transaction updates

Bulk card generation

These tools help businesses automate financial workflows.

Multi-BIN Support

Platforms offering multiple BIN ranges improve acceptance across regions.

This helps:

Reduce decline rates

Improve international compatibility

Support global merchants

Increase payment reliability

Multi-BIN availability is especially useful for cross-border payments.Scalable Infrastructure for Growing Businesses

Businesses handling large volumes of payments require reliable systems.

Scalable issuing platforms support:

High-volume transactions

Rapid user growth

Multiple currencies

Global operations

This ensures long-term system performance.

Conclusion

Card issuing APIs are transforming how businesses create, manage, and automate payment systems. By enabling instant virtual card generation and real-time financial tracking, these tools reduce manual work and improve operational efficiency.

As digital payments continue to expand in 2026, businesses that integrate card issuing APIs into their infrastructure gain greater flexibility, stronger financial control, and improved scalability across global operations.

Understanding how card issuing APIs work—and selecting the right platform—can significantly impact payment performance, automation capabilities, and long-term growth.