The demand for embedded financial services continues to grow, and companies across industries are looking to integrate payments directly into their products. One of the most practical ways to achieve this is to launch a virtual card program, allowing businesses to issue payment cards to employees, customers, or partners.

In 2026, launching a card program no longer requires building banking infrastructure from scratch — but it still involves several critical components, including compliance, partnerships, and technical integration.

This guide walks through how a virtual card program works, the key building blocks involved, and the exact steps needed to launch successfully.

What Is a Virtual Card Program

A virtual card program enables a business to issue digital payment cards that operate on major networks such as Visa or Mastercard. These cards can be used for online payments, subscriptions, advertising spend, or internal expense management.

Unlike physical cards, virtual cards are generated instantly and can be customized for specific use cases.

Typical features include:

-

Unique card numbers for each user or transaction

-

Spending limits and controls

-

Real-time transaction monitoring

-

Integration with software platforms via APIs

-

Support for global online payments

Virtual card programs are widely used in fintech, SaaS platforms, marketplaces, and enterprise expense systems.

Key Components: BIN Sponsorship, Issuer, Processor

Launching a virtual card program requires coordination between several financial entities.

BIN Sponsorship

A Bank Identification Number (BIN) sponsor is a licensed financial institution that enables your program to operate on card networks. Without a BIN sponsor, cards cannot be issued legally.

Issuing Bank

The issuing bank holds the funds backing the cards and ensures compliance with financial regulations.

Payment Processor

The processor connects your system to card networks and handles transaction authorization, clearing, and settlement.

Program Manager or Platform

Modern businesses often rely on a platform that aggregates these components into a single solution, reducing complexity and time to market.

Understanding these roles is essential before selecting a provider.

Steps to Launch a Virtual Card Program

While implementation details vary, most programs follow a structured process.

Step 1 — Define Your Use Case

Identify how the cards will be used:

-

Employee expenses

-

Customer payouts

-

Advertising payments

-

Subscription management

This determines compliance requirements and technical design.

Step 2 — Choose a Platform or Partner

Select a provider that offers issuing capabilities, API access, and global coverage.

Step 3 — Complete Onboarding and Compliance

Provide required business documentation and complete verification processes.

Step 4 — Fund Your Program

Deposit funds into the program account to back issued cards.

Step 5 — Integrate APIs or Use Dashboard

Developers can integrate APIs for automation, or teams can manage cards manually via a dashboard.

Step 6 — Issue Virtual Cards

Create cards for users, teams, or specific transactions with defined limits and rules.

Step 7 — Monitor and Optimize

Track transactions, adjust spending controls, and optimize program performance over time.

Compliance and Regulatory Considerations

Financial services are heavily regulated, and card programs must meet strict requirements.

KYC and KYB Requirements

Businesses and, in some cases, end users must be verified.

PCI DSS Compliance

Cardholder data must be handled securely according to industry standards.

Anti-Money Laundering (AML)

Programs must monitor and report suspicious activity where required.

Regional Regulations

Different jurisdictions impose varying rules on card issuing and payment processing.

Working with an established platform helps ensure these requirements are managed effectively.

Launching Faster with Buvei Infrastructure

For businesses seeking to reduce complexity and accelerate deployment, Buvei provides a streamlined approach to virtual card issuing.

Simplified Setup

Virtual cards can be created quickly after account registration and funding, without lengthy setup processes.

Multi-BIN Support

Access to multiple BIN regions allows businesses to optimize payment acceptance globally.

Stablecoin Funding

Programs can be funded using USDT (TRC20/ERC20), offering faster and potentially lower-cost cross-border transactions.

Broad Platform Compatibility

Cards are designed for use across major online platforms, including advertising networks and SaaS services.

Centralized Management

Multiple cards can be issued and managed within a single interface, supporting team-based operations.

How to Get Started with Buvei (Step-by-Step)

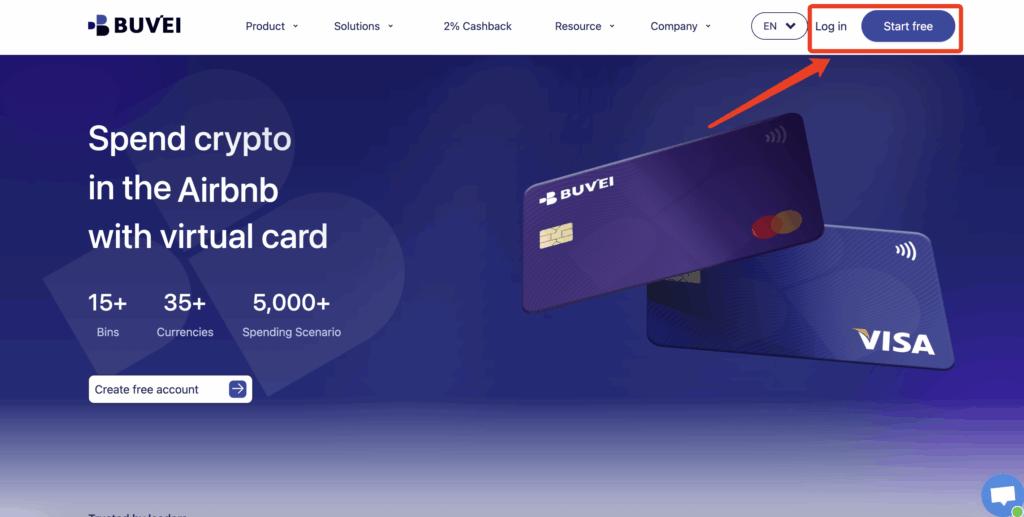

Step 1 — Register a Buvei Account

Visit https://buvei.com

Create a free account and complete email verification. After verification, log in to access the Buvei dashboard.

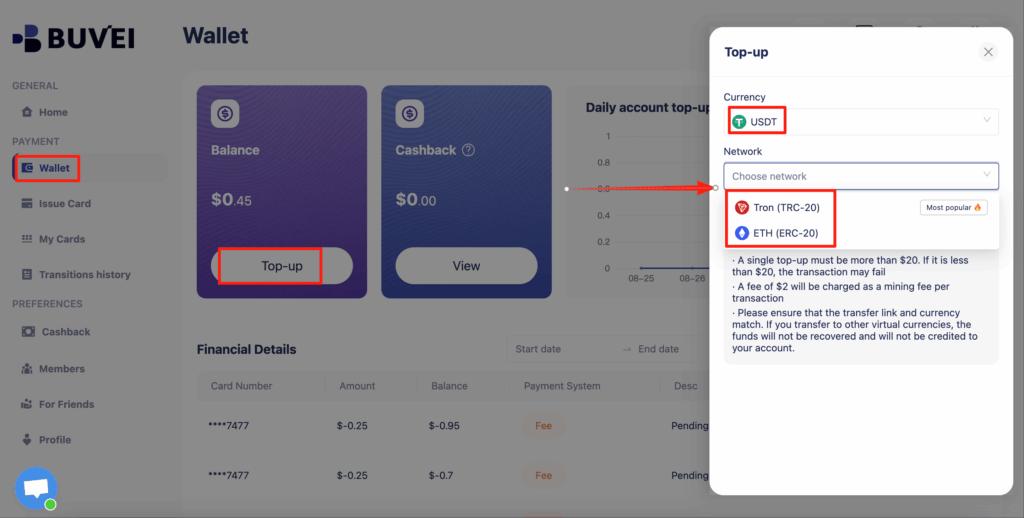

Step 2 — Fund Your Wallet

Navigate to the Wallet tab.

-

Deposit USDT via TRC20 or ERC20

-

Copy your deposit address

-

Transfer funds from your crypto wallet or exchange

-

Wait for confirmation

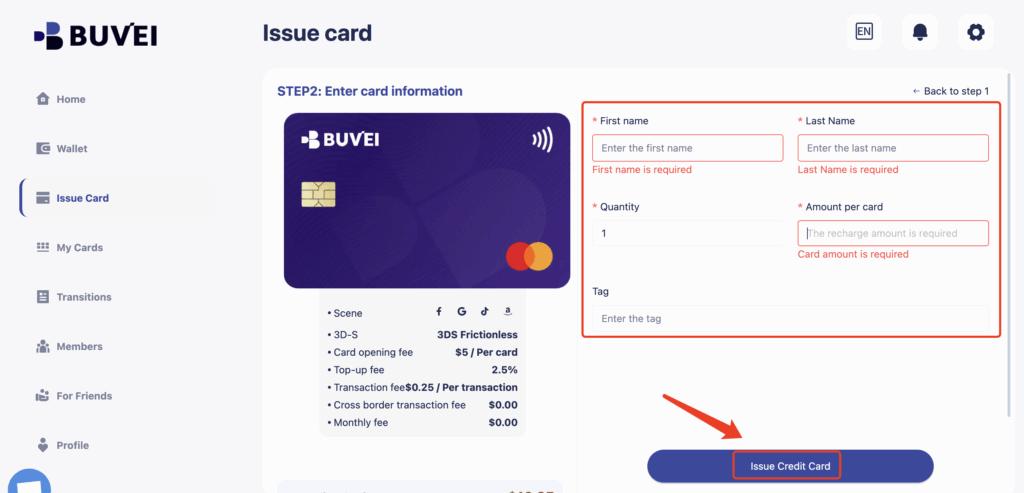

Step 3 — Create Virtual Cards

Go to the Cards section.

Select your preferred BIN region (U.S. BIN recommended)

Quick Setup for White-Label Card Programs

Choose card type

Enter card details — name, amount, and quantity

Click Issue Card

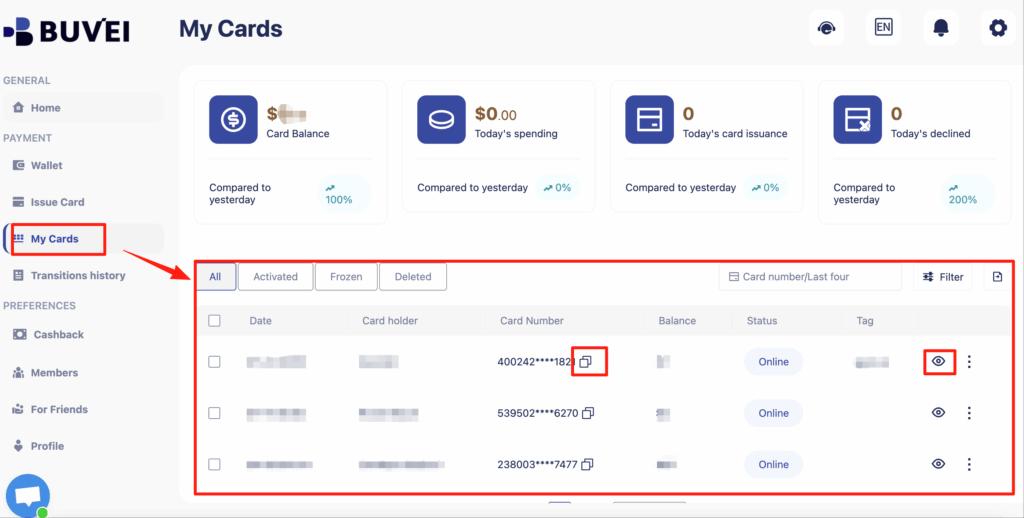

Step 4 — Manage Cards

Under My Cards, you can view:

-

Card number

-

Expiration date

- CVV

-

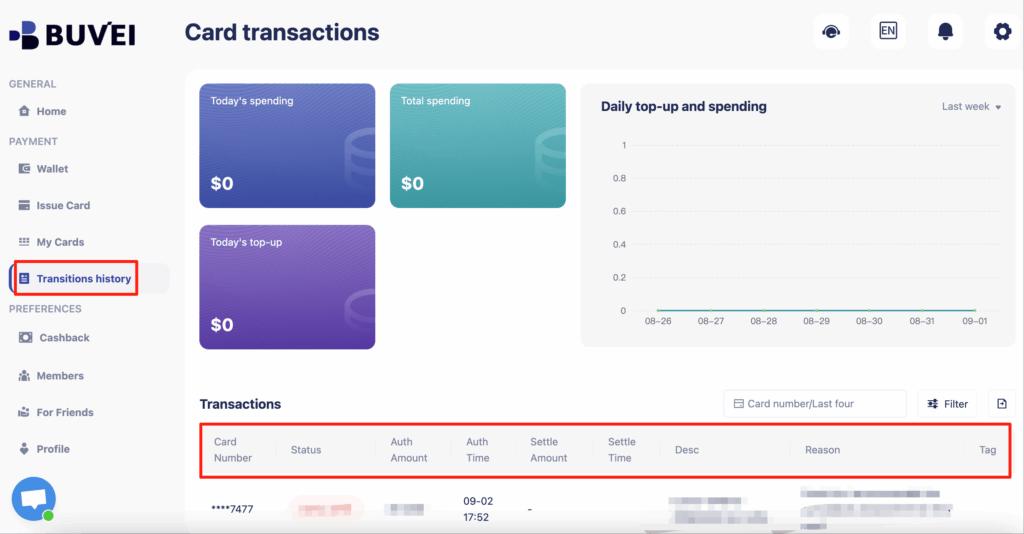

Transactions and balances

Cards are ready for immediate use across supported platforms.

Final Thoughts

To launch a virtual card program successfully, businesses must understand both the technical and regulatory landscape. While the process once required significant resources and banking relationships, modern platforms have simplified deployment dramatically.

By leveraging existing infrastructure, companies can focus on building products rather than managing financial complexity. For organizations seeking speed, flexibility, and global payment capability, solutions such as Buvei provide a practical path to launching and scaling virtual card programs efficiently.