As subscription services, global e-commerce, and online payments expand, interest in the free virtual Visa card has surged. These digital cards allow users to make payments without exposing their primary banking information, offering a practical balance of convenience and security. In 2025, more platforms provide free or near-free virtual cards designed for everyday online payments, app store purchases, digital services, and trial subscriptions.

This guide explains how free virtual Visa cards work, which providers offer them, how to apply, and how to use them responsibly while ensuring your financial information stays protected.

The Growing Role of Virtual Visa Cards in 2025

Virtual Visa cards have shifted from niche tools to mainstream financial products. Their rise is driven by several factors:

1) Online subscription growth

Streaming services, cloud software, and gaming platforms increasingly operate on recurring billing. A virtual Visa card gives users better control over renewals and spending limits.

2) Global e-commerce expansion

More consumers purchase from international platforms. Virtual cards with multi-currency support simplify cross-border payments while reducing fraud exposure.

3) Improved security and privacy

Since a virtual card doesn’t reveal a physical card number, it reduces the risk of data theft. Some 2025 platforms also offer single-use card numbers, adding an extra layer of protection.

4) Rapid issuance and easy access

Many digital finance apps allow users to create a free virtual Visa card instantly, without visiting a bank or waiting for physical mail.

What “Free” Really Means for Virtual Visa Cards

When a service advertises a free virtual Visa card, it typically refers to one or more of these features:

1) Free issuance

Most fintech apps now generate the digital card at no cost.

2) No monthly fees

Some providers remove maintenance charges as long as the account remains active.

3) No minimum balance requirement

You can create the card without depositing a large initial amount.

4) Potential hidden costs

While issuance may be free, users may still encounter:

-

Currency conversion fees

-

Top-up charges depending on funding method

-

International transaction fees

-

Optional premium features

Understanding these points helps users evaluate whether a card is genuinely free for their intended usage.

Reliable Platforms Offering Free Virtual Visa Cards in 2025

Below are mainstream categories of providers known for offering low-cost or free virtual Visa cards. To maintain credibility, descriptions focus on general features rather than unsupported claims.

1) Digital banks

Many modern online banks issue free virtual Visa cards linked to a digital checking or spending account. These institutions often support real-time fraud alerts and freeze/unfreeze functions.

2) Fintech payment apps

Apps specializing in cross-border payments or spending controls typically offer free or low-fee virtual cards. They appeal to users seeking budget management tools or secure online shopping methods.

3) Prepaid virtual Visa providers

Some prepaid card issuers generate free virtual Visa numbers after initial account setup. These are commonly used for subscriptions, trial services, and controlled spending.

4) International finance platforms

Several global financial apps provide virtual Visa cards as part of their digital wallet system. Their advantages include multi-currency support and widespread merchant acceptance.

When evaluating any platform, users should verify:

-

Supported countries

-

Accepted funding methods

-

Fee schedule

-

Usage limits

-

Customer service availability

This ensures the chosen card aligns with real payment needs.

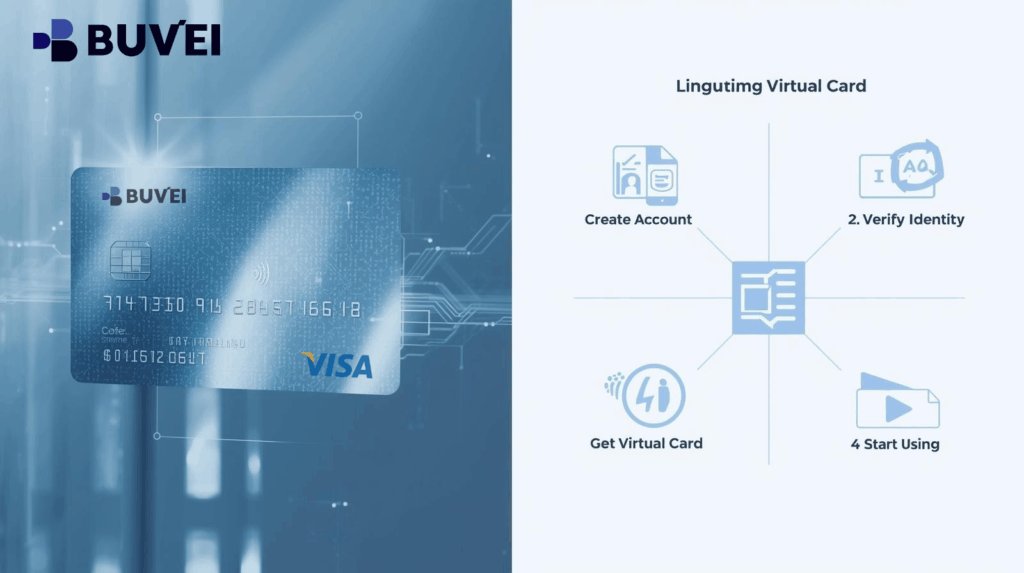

How to Apply for a Free Virtual Visa Card in 2025

Although each provider's interface differs, the overall process is consistent across platforms:

Step 1: Create an account

Download the app or access the provider’s portal. You’ll need a valid mobile number or email address.

Step 2: Complete identity verification

Even free virtual Visa cards often require KYC verification to comply with financial regulations. This may include submitting identification documents.

Step 3: Generate your virtual Visa card

Once approved, the system creates your card instantly. You’ll receive:

-

Card number

-

Expiration date

-

CVV

These can be used for online purchases immediately.

Step 4: Fund your virtual card

Depending on the provider, you may fund the card by:

-

Bank transfer

-

Debit card

-

Credit card

-

Digital wallet

Some providers allow use without an initial deposit for subscriptions or small-value transactions.

Step 5: Start using your card

You can now use the card for:

-

Online shopping

-

App store purchases

-

Streaming services

-

Trial subscriptions

-

Digital products

This process typically takes only a few minutes from start to finish.

Best Practices for Safe Use of Virtual Visa Cards

Although virtual Visa cards are inherently secure, users should still follow good digital hygiene practices.

1) Enable spending limits

Many platforms allow per-transaction or daily limits. Setting these helps prevent unauthorized large charges.

2) Use single-use or disposable numbers (if available)

These dynamically generated numbers are ideal for unfamiliar websites or one-time purchases.

3) Monitor statements regularly

Even small unauthorized transactions can indicate card compromise.

4) Avoid storing your card unnecessarily

Unless required, avoid saving card details in multiple online platforms to reduce exposure.

5) Use two-factor authentication

Adding another security layer protects your financial data during login and payment approval.

6) Read the provider’s fee schedule carefully

Hidden charges are a common issue for virtual cards marketed as “free.” Understanding fees prevents unexpected deductions.

When a Free Virtual Visa Card May Not Be Enough

While free virtual Visa cards work well for most online payments, there are scenarios where they fall short:

1) Large or high-risk transactions

Some providers limit transaction amounts or block specific merchant categories.

2) Recurring international subscriptions

Currency conversion or cross-border fees may accumulate over time.

3) In-person purchases

Virtual cards typically lack physical tap-to-pay functionality unless paired with a digital wallet.

4) Business-level usage

Companies often require higher transaction limits, multi-user access, or advanced accounting integrations beyond what a free virtual card can offer.

In such cases, users may need upgraded features, a physical card, or a business-oriented account.

Conclusion

The free virtual Visa card has become an essential tool for safer, more flexible online payments in 2025. Whether you're signing up for trial subscriptions, shopping globally, or protecting your banking details, virtual cards offer a reliable balance of security and convenience.

By choosing reputable providers, understanding fee structures, and maintaining smart digital habits, users can take full advantage of these modern payment tools. A well-selected virtual Visa card can simplify online spending and reduce financial risks significantly.